Published in this month’s “The Threshold,” the American Bar Association’s merger-focused quarterly journal:

Andreas Stargard [1]

Fittingly for this publication, international merger control poses a threshold problem. One may call it the “zero-threshold contagion.” On January 14, 2013, it spread to the newest member of the growing number of worldwide merger-control regimes: the victim in this particular instance was COMESA[2] – a multi-jurisdictional body with a vast geographic span across 19 eastern and southern African economies, home to a population 25% larger than that of the United States.

Background

With the inception of the COMESA Competition Commission’s (“CCC”) operations, certain corporate transactions “with a regional dimension” are now subject to mandatory merger notification. Whether or not this notification requirement has a suspensory effect on the notified transaction[3] is but one of the many ambiguities pervading the young merger regime, which applies a “substantially prevent or lessen competition” test, in addition to other, less-common criteria for merger analysis. A fair question arises: “What exactly are the rules?”

Much of the commentary on the CCC’s emergence has been critical, mostly focused on the many ambiguities in the system, and occasionally going as far as questioning the agency’s mandate, competence, and extraterritorial reach. This article lays out the objective underlying facts behind COMESA, which are often little understood.

Having a merger-control regime – more broadly speaking, a competition law[4] – in the region is neither surprising nor a sudden development. The statute has been in existence for a decade, and the advent of the CCC merely represents the pinnacle of a rather long regional history that was to lead, quite predictably, to its implementation.

To understand the impetus behind this final chapter in the gestation of supra-national antitrust law in Africa, it helps briefly to recall COMESA’s history. Its goals were premised ab initio on economic progress in the region, having evolved from its precursor “Preferential Trade Area for Eastern and Southern Africa” (1981) into the COMESA of today (1994). COMESA’s establishing Treaty, drafted two decades ago, left no doubt that competition law would become a key focus area for the organization.[5] After all, one of COMESA’s primary stated goals is a “wider, harmonised and more competitive market.”[6]

It is against this historical backdrop that the organization enacted its Competition Regulations and Rules in 2004. Yet, a decade later, the Regulations remained empty legislative vessels, as there was no enforcement body to apply them.[7] Elsewhere, I have called the phenomenon of the gap between existing antitrust legislation and its lack of enforcement the “missing policeman rubicon.” The COMESA competition regime finally crossed that river when the CCC, headquartered in Malawi, became operational in January of this year under the leadership of George Lipimile. Its launch finally awakened the dormant antitrust statute and its merger-control regime.

From tabula rasa to Established Enforcement – a Rocky Road without a Threshold

Almost a year into the CCC’s existence, one may ask how the various pieces of the enforcement puzzle have come together? Filling in the blank canvas on which Mr. Lipimile’s agency is building its administrative platform has not come without hiccups, as well as numerous pragmatic questions raised about how COMESA will achieve its stated mission. First and foremost among these is the threshold question.

As readers of this publication are keenly aware, when advising clients on the perennial question of “where must we file,” law firms commonly operate on the basis of a piece of coveted and fiercely guarded work product, created over the course of decades and regularly updated, in all likelihood, by a junior attorney: in short, a jurisdictional matrix showing key variables such as per-party deal-value or revenue thresholds, (disfavored) market-share tests, exceptional minority shareholding or control rules, and other unique characteristics of each of the ten dozen or so merger regimes currently in operation worldwide.

It is a safe bet that the attorneys who had the misfortune of having to add the COMESA section to their firm’s matrix in early 2013 were scratching their heads at the (then virtually unexplained) language governing CCC merger enforcement. Their first question was: What’s the revenue threshold? Short answer: None.

The statute requires parties to have combined worldwide and regional aggregate revenues or assets, whichever is higher, of at least “COM$ Zero.”[8] The CCC’s explanation for this de facto non-existent threshold has been that “different Member States are at different levels of economic development and hence a realistic threshold can only be determined after the Regulation has been tested on the market. Therefore, the threshold shall be raised after a period of implementation of the Regulations.”[9]

In addition to the threshold issue, it has also remained unhelpfully vague what it means for a business to “operate” within COMESA – e.g., are mere import sales sufficient? How many of the parties to the transaction must be commercially active in the common market? Does a COMESA notification discharge all filing obligations vis-à-vis member-state competition authorities, even those whose markets are primarily affected by a given transaction (i.e., is the CCC a true one-stop-shop)? Are acquisitions of minority shareholdings out of scope? How is the (seemingly unduly steep) filing fee actually calculated?

In brief, the need for significant clarification was abundantly clear early on. To its credit, the CCC did follow international best practices and released its explanatory Guidelines in draft form for public comment in April. The Guidelines cover not only the procedural steps and substantive analysis applied by the agency, but also some of the uniquely regional topics, e.g., the “public interest criterion” under Article 26 of the Regulations – an additional analytical (most would say solely socio-political) criterion that goes far beyond orthodox antitrust principles, muddying the waters of pure merger-control assessment and arguably diluting outcome predictability to the point of a “black box.” In response, commentators from across the globe (including the American Bar Association) provided their critical response during the summer, in the hopes of ensuring the young agency’s smooth evolution from blank slate to rational and proportionate merger enforcer.

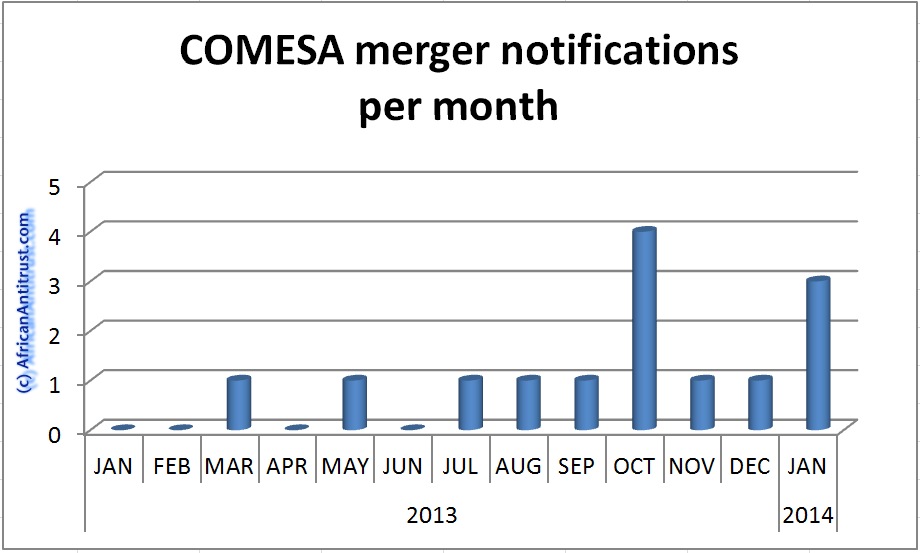

It is now – almost one year into the COMESA competition saga – ever more evident that significant confusion (and parties’ resulting aversion to filing) remains. One piece of readily available empirical evidence demonstrating this fact is the lack of any meaningful number of merger notifications. It is no secret that many private practitioners follow the rule that, in the absence of clarity and meaningful thresholds, COMESA simply constitutes “no-go territory” for merging firms. Such advice has led not only to an instinctive discounting of COMESA’s relevancy, but also directly to the CCC’s subdued statistics: the agency has received only nine ten notifications in the first ten eleven months of its existence. Compare this rate (which averages less than one per month) to the estimated number of filings received by another relatively young antitrust watchdog in a developing economy, the Indian Competition Commission (which has received more than 5 notifications per month).

In short, the view persists among global competition counsel that parties can, in commercial practice, simply dispense with a CCC filing that would otherwise be technically required. Weighing the risk of non-notification (“Is the CCC willing to bring an enforcement action for failure to notify?” – “Does it have adequate resources to sue?”) against the costs, burden and unpredictability of doing so has, in practice, often resulted in a decision not to notify.

This attitude, in turn, revives the dilemma of the “missing policeman”: even if he is physically present, an enforcer who lacks authoritative presence will remain ineffectual – a danger that is only aggravated if the rules he is to apply are not clearly laid out.

The lackluster statistics also raise the further question whether COMESA simply “bit off too much” on the merger-control front, especially when one considers its zero-dollar thresholds, small staff, fragmented supra-national infrastructure, and other factors that call into question its viability (e.g., jurisdictional disputes with some of its member states). In 2012, senior outside advisers had warned the CCC that – with a zero-dollar threshold and almost no nexus requirement – it was either going to be flooded with de minimis notifications or receive virtually none whatsoever, as parties would simply ignore the mandate. Thus far, the latter has turned out to be the case.

COM$0, No Nexus, and a Hefty Price Tag – Recipe for Disaster?

The zero-threshold dilemma ranks perhaps as the most significant among the criticisms leveled at the CCC. Yet, it does not stand alone in the confusing arsenal of statutory language that routinely perplexes counsel advising merging parties with commercial activities in the region.

Lack of Clear Jurisdictional Nexus

At present, a merger transaction[10] is technically notifiable where only one of the parties operates within more than one member state of the common market. This sets the stage for perverse possibilities: a transaction with a target jurisdiction that, to this day, does not have a domestic antitrust law will nonetheless require a CCC notification with its attendant colossal filing fee. Worse, the same goes for the acquisition of a target that has no operations whatsoever within COMESA, but where the acquirer alone operates in two member states.

A prime real-life example is the recent COMESA approval of Total’s acquisition of Shell’s Egyptian gas operations.[11] Pursuant to the terms of the published decision – which is marred by the omission of crucial terms, thereby rendering a meaningful interpretation difficult – the CCC determined “that the transaction has a regional dimension in that both [sic!] the acquiring firm operate [sic!] in more than one COMESA Member State.”[12] Is it both or just one? The decision proceeds to identify only the states in which the acquirer is active and does not mention those in which the target has any cognizable operations. In yet another notified transaction, only the acquiring party had operations in three member states, whereas the target was admittedly “only active in Nigeria, and has no operations in any of the COMESA Member States.”[13]

In essence, under the present regime, even transactions with a de minimis nexus to the region are subject to notification – a rather blatant jurisdictional overreach when compared to international best practices, as enunciated for instance by the ICN in its Recommended Practices for Merger Notification Procedures or in the OECD’s counterpart guidance. These provide for the generally accepted principle that the parties’ commercial activities on the relevant market must have a material nexus to the reviewing jurisdiction, i.e., the merger must be likely to cause an appreciable competitive effect within the territory of the reviewing jurisdiction, such that notifications are only required for “those mergers that have an appropriate nexus with their jurisdiction.”[14]

In its present form, the net cast by the COMESA merger regulations is woven far too finely, as it catches transactions in which only the acquirer operates in the Common Market. Should the status quo persist through the next iteration of the merger rules’ amendments, the CCC will entrench itself as being out of sync with accepted best practices and will have cemented an inopportune example of extraterritorial overextension in global merger enforcement.

A (Pricey) Tollbooth on the African Merger Interstate

Other areas of criticism may sting even more, however. A two-fold key problem of the young merger regime has been (1) its confusingly worded filing-fee provision and (2) the perceived exploitation thereof by the CCC. Tackling these briefly in turn, it is almost an understatement to call the fee provision[15] ambiguous or unclear – its indiscriminate use of “higher of” vs. “lower of,” with no transparent identification of the relevant reference points, is a prime example of avoidably poor legislative drafting.

The publication of a barrage of (incorrect, as it turns out) news flashes and client alerts by law firms prompted the CCC, to its credit, to issue corrective guidance shortly after its inception: on February 26, 2013, it clarified that the half-million-dollar figure was in fact the maximum filing fee.[16] In the words of the CCC: “When a merger is received, the [CCC] will first calculate 0.5% of the combined turnover of the merging parties. [It] will then calculate 0.5% of the combined value of assets of the merging parties. [It] will then compare results in 1 and 2 above and get the higher value. [It] will then compare this higher value to the COM$500,000.”[17]

As a practitioner’s rule of thumb, if the combined annual revenues or asset values of the notifying parties are (U.S.) $100 million or more, the administrative fee will be the maximum $500,000.

The agency’s clarification notwithstanding, it goes without saying that the resulting fees (including miscellany)[18] will nonetheless be exorbitant. The filing fee alone is vastly disproportionate to the deal values of all but the largest transactions. Indeed, it constitutes by far the highest merger notification fee in the world (keeping in mind that the global filing-fee scale ranges from the EU’s €0 fee to the United States’ $280,000 maximum).

According to a March 2013 CCC letter, the agency undertook a “preliminary assessment” of expected notification fees, concluding that the cost of a (presumably one-stop-shop) COMESA filing would be “much lower than that of the national competition authorities and this has resulted in the cost of doing business (notifying using the COMESA route) being reduced by about 43.4%.”[19] It admits, however, that this early estimate was just that – a guess, as it had “not yet concluded any merger investigation for one to have a basis for any comparisons.”[20]

Since then, the CCC has nonetheless taken full advantage of its “tollbooth” role. For instance, as reported in various business journals,[21] it billed the parties to the pharmaceutical Cipla transaction at the maximum level possible, cashing in half a million U.S. dollars in the process. It is difficult to recreate the CCC’s unstated methodology of its “preliminary assessment,” but under no hypothesis would the Cipla parties’ national filing fees have matched, much less exceeded, the COMESA fee.

Recalling that one of the stated goals of COMESA is to create a “more competitive market,” one may ask whether the organization has lost its way? Is it spitefully naïve or rather sadly perceptive to view the creation of the CCC as a short-sighted attempt by a developing region to extract a de facto tax on local businesses and foreign corporations interested in acquiring them – in effect thereby stifling regional growth and outside investment?

Sources who were present during preparatory meetings between CCC staff and international advisors from other enforcement agencies and academia confirm that, even prior to its becoming operational, the CCC affirmatively counted on taking full advantage of the high fees, perceiving them to be a source of funding elementary to the agency’s existence. This anticipated revenue stream was viewed as so significant that members of the Kenyan Competition Authority (“CAK”) and the CCC engaged in an open quarrel over the ultimate recipient thereof and whether there would be any fee split among NCAs and the CCC. This type of internal common-market discord eventually led to a “revenue-sharing agreement” of sorts.[22] Yet, Kenya and COMESA have subsequently continued to disagree on whether COMESA has jurisdiction over certain notifiable transactions – leading to further ambiguity over whether COMESA will be a true “one-stop-shop”. It stands to reason that the agencies’ prior fee dispute is but one reason for the CAK’s formal request for a “cooperation framework” between the authorities, in order to “operationalize” the two agencies’ joint mandate and to “actualize the interface.”[23]

Going Forward – Mixed Signs of Hope, But the Window is Closing

The silver lining amid clouds of confusion and disagreement surrounding COMESA’s merger-control provisions consists of universal anticipation of revamped legislation and guidance papers. Since it is the most obvious shortcoming, the glaring zero-threshold provision will likely take center stage at the upcoming annual meeting of the COMESA Council, slated for December, which unites cabinet-level emissaries from all 19 member states. The Council alone can amend the rules and regulations governing the CCC. The agency, however, is presumptively in sole charge of its interpretive guidance relating to the legislation. To date, the agency has not published a final version of its Guidelines. It is therefore too early to conclude whether the submission of comments on the drafts by experienced practitioners and other experts has borne fruit.

In addition, while the public consultation procedure on the Regulations is well-intentioned in principle, its delayed start and lengthy duration indicate a protracted period of uncertainty and, thus, the continuing validity of inadequate legislation, i.e., the status quo. The consultation’s implementation, effectiveness, and quality of outside advisers also remain to be determined.

In sum, COMESA’s competition enforcement has left many questions unanswered. The low number of actual merger notifications is a direct reflection of parties’ and practitioners’ unease at dealing with the CCC. Crucial elements of the agency’s ultimate success will almost certainly include the clarification of its existing rules as well as the adaptation of its merger legislation to real-life exigencies, such as fundamentally inverting the current ratio of high filing fees and low thresholds.

[1] Andreas Stargard is a partner in the Brussels office of Paul Hastings.

[2] “Common Market for Eastern and Southern Africa,” of whose 19 members only a minority of jurisdictions currently have domestic antitrust laws (Egypt, Kenya, Malawi, Mauritius, Seychelles, Swaziland, Zambia and Zimbabwe). Notably, COMESA excludes South Africa, by far the largest economy in the region, which has its own merger control regime.

[3] The COMESA Regulations do not clearly provide for a prohibition on closing prior to clearance, although the formal Notification Form (No. 12) contains language indicating suspensory effect. CCC’s staff has made informal comments at various conferences stating that the regime was not suspensory. However, the last legislative word has not been spoken on the issue, or if it has, it remains ambiguous.

[4] This article focuses on the merger-control aspect not only because it is the Threshold’s topical focus. COMESA’s broader antitrust rules (on abuse of dominance or cartel prohibition) are not yet fit subjects for comment, as they have simply not seen any application in practice as of this writing.

[5] See, e.g., COMESA Treaty Art. 55 (establishing a regional competition law framework and foreshadowing implementing Regulations); Art. 52 (prohibiting certain types of state aid, “which distorts or threatens to distort competition by favouring certain undertakings or the production of certain goods”); Art. 54 (anti-dumping); see also Arts. 76, 85, 86, 99, 106.

[8] A so-called “COMESA dollar” is a monetary accounting unit pegged (since May 1997) to the U.S. dollar at a fixed 1-to-1 exchange rate.

[9] Draft Merger Assessment Guideline, §1.3.

[10] That is, the “direct or indirect acquisition or establishment of a controlling interest by one or more persons in the whole or part of the business of a competitor, supplier, customer or other person.” Art. 23 COMESA Competition Regulations

[14] OECD Recommendation of the Council on Merger Review I.A.1.2.i.

[15] Rule 55(4) of the amended COMESA Competition Rules reads as follows: “Notification of a notifiable merger shall be accompanied by a fee calculated at 0.5% or COM$500000, or whichever is lower of the combined annual turnover or combined value of assets in the Common Market, whichever is higher.”

[16] The “greater of” calculus in the provision instead refers to the half-percent of “assets” versus “revenues,” according to the CCC.

[18] Fees for notifications are not the only party-sponsored revenue source, as the November 2012 amendments to the Competition Rules also prescribe a $10,000 fee each for applications for authorization and for exemption orders. See Amended Rules 63(1) and 77(4).

[23] February 14, 2013 letter from CAK Director-General Kariuki to the CCC’s Mr. Lipimile. The Kenyan Attorney General subsequently issued a ruling against COMESA jurisdiction over certain Kenyan transactions in March 2013. See https://africanantitrust.com/2013/03/15/

Ms. Weeks-Brown noted the rise of pan-African (vs. purely domestic) banks, observing the added benefit of improved competition, as well as the steady rise of fintech on the continent. The latter is especially important as the continent is still

Ms. Weeks-Brown noted the rise of pan-African (vs. purely domestic) banks, observing the added benefit of improved competition, as well as the steady rise of fintech on the continent. The latter is especially important as the continent is still

According to the South African Competition Commissioner, Mr Tembinkosi

According to the South African Competition Commissioner, Mr Tembinkosi