East-Africa & Antitrust: Enforcement of EAC Competition Act

By AAT guest author, Anne Brigot-Laperrousaz.

Introduction: Back in 2006…

The East African Community (the “EAC”) Competition Act of 2006 (the “Act”) was published in the EAC Gazette in September 2007. The Act was taken as a regulatory response to the intensification of competition resulting from the Customs Union entered into in 2005. This was the first of the four-step approach towards strengthening relations between member States, as stated in Article 5(1) of the Treaty Establishing the EAC.

Challenges facing the EAC

As John Oxenham, an Africa practitioner with advisory firm Pr1merio, notes, “10 years have passed since the adoption of the EAC Act, yet it remains unclear when (and if) the EAC will develop a fully functional competition law regime.”

The EAC Competition Authority (the “Authority”) was intended to be set up by July 2015, after confirmation of the member States’ nominees for the posts of commissioners. Unfortunately Rwanda, Uganda and Burundi failed to submit names of nominees for the positions available, and the process has become somewhat idle, leaving questions open as to future developments.

The main challenges facing the EAC identified by the EAC’s Secretariat is firstly, the implementation of national competition regulatory frameworks in all member States; and secondly, the enhancement of public awareness and political will[1].

The first undertaking was the adoption of competition laws and the establishment of competition institutions at a national level, by all member states, on which the sound functioning of the EAC competition structure largely relies.

Apart from Uganda, all EAC member States have enacted a competition act, although with important discrepancies as to their level of implementation at a national level.

The second aspect of the EAC competition project is the setting up of the regional Competition Authority, which was to be ensured and funded by all members of the EAC, under the supervision of the EAC Secretariat. Although an interim structure has been approved by member States, the final measures appear to be at a deadlock.

As mentioned, the nomination of the commissioners and finalisation of the setting up of the EAC Competition Authority came to a dead-end in July 2015, despite the $701,530 was set aside in the financial budget to ensure the viability of the institution[2]. It is widely considered, however, that this amount is still insufficient to ensure the functionality of the Competition Authority. Andreas Stargard, also with Pr1merio, points out that “[t]he EAC has been said to be drafting amendments to its thus-far essentially dormant Competition Act to address antitrust concerns in the region. However, this has not come to fruition and work on developing the EAC’s competition authority into a stable body has been surpassed by its de facto competitor, the COMESA Competition Commission.”

Furthermore, inconsistencies among national competition regimes within the EAC are an important impediment to the installation of a harmonised regional enforcement. Finally, international reviews as well as national doctrine and practice commentaries have highlighted the lack public sensitization and political will to conduct this project.

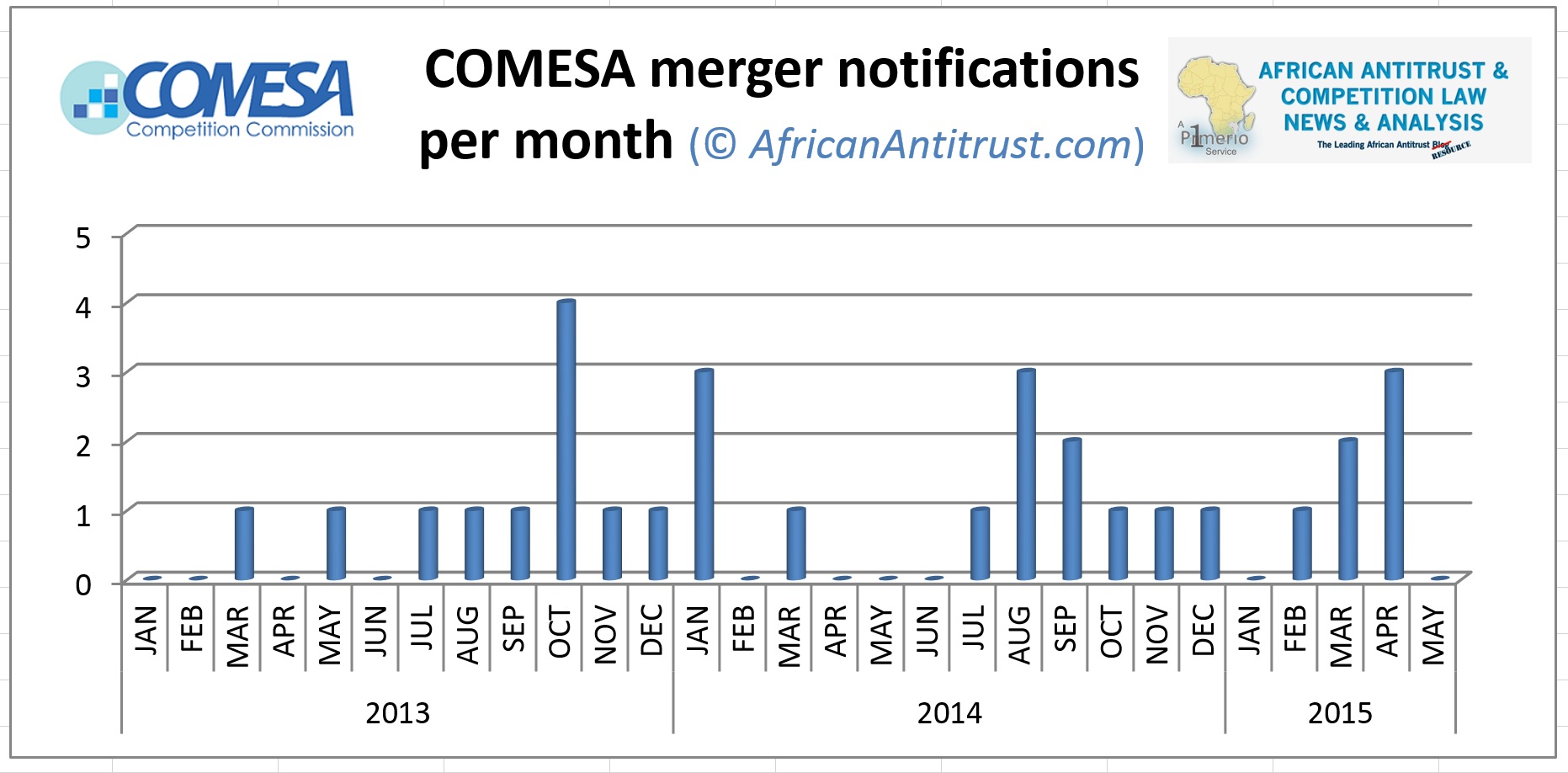

A further consideration, as pointed out by Wang’ombe Kariuki, Director-General of the Competition Authority of Kenya, is the challenge posed by the existence of the Common Market for Eastern and Southern Africa (“COMESA”).

Conclusion

The implementation of the EAC has not seen much progress since its enactment, despite its important potential and necessity[3]. It therefore remains to be seen how the EAC deals with the various challenges and whether it will ever become a fully functional competition agency.

A quick summation of the status of the national laws of the various EAC members can be seen below. For further and more comprehensive assessments of the various member states competition law regimes please see African Antitrust for more articles dealing with the latest developments.

EAC Member States Status

Tanzania

The Tanzanian Fair Competition Act (the “FCA”) was enacted in 2003, along with the institution of a Commission and Tribunal responsible for its enforcement. The FCA became operational in 2005. Tanzania’s competition regime was analysed within the ambit of an UNCTAD voluntary peer review in 2012[4]. The UNCTAD concluded that Tanzania had overall “put in place a sound legal and institutional framework”, containing “some of the international best practices and standards”.

This report, however, triggered discussions on major potential changes to the FCA, which would impact, in particular, institutional weaknesses and agency effectiveness[5]. One of the most radical changes announced consisted in the introduction of criminal sanctions against shareholders, directors and officers of a firm engaged in cartel conduct[6], although there is no sign that this reform will be adopted.

Kenya

Kenya, following a 2002 OECD report[7] and the European Union competition regulation model, replaced its former legislation with the 2010 Competition Act, which came into force in 2011, and established a Competition Authority and Tribunal. Under the UNCTAD framework, the 2015 assessment of the implementation of the recommendations made during a voluntary peer review conveyed in 2005[8] was generally positive. It was noted, however, that there was an important lack of co-operation between the Competition Authority and sectoral regulators, and that there was a need for clear merger control thresholds[9].

Burundi

Burundi adopted a Competition Act in 2010, which established the Competition Commission as the independent competition regulator. To date, the Act has not yet been implemented, and accordingly no competition agency is in operation[10].

A 2014 study led by the Burundian Consumers Association (Association Burundaise des Consommateurs, “Abuco”) (which was confirmed by the Ministry of Trade representative) pointed to the lack of an operating budget as one of the main obstacles to the pursuit of the project[11].

Rwanda and Uganda

Rwanda enacted its Competition and Consumer Protection Law in 2012, and established the Competition and Consumer Protection Regulatory Body.

As for Uganda, to date no specific legal regime has been put in place in Uganda as regards competition matters, although projects have been submitted to Uganda’s cabinet and Parliament, in particular a Competition Bill issued by the Uganda Law Reform Commission, so far unsuccessfully.

Footnotes:

[1] A Mutabingwa “Should EAC regulate competition?” (2010), East African Community Secretariat

[2] C Ligami, “EAC to set up authority to push for free, fair trade” (2015), The EastAfrican

[3] O Kiishweko, “Tanzania : Dar Praised for Fair Business Environment” (2015), Tanzania Daily News

[4] UNCTAD “ Voluntary Peer Review on competition policy: United Republic of Tanzania” (2012), UNCTAD/DITC/CLP/2012/1

[5] S Ndikimi, “The future of fair competition in Tanzania” (2013), East African Law Chambers

[6] O Kiishweko, “Tanzania: Fair Competition Act for Review’ (2012), Tanzania Daily News.

[7] OECD Global Forum on Competition, Contribution from Kenya, “ Kenya’s experience of and needs for capacity building/technical assistance in competition law an policy “ (2002), Paper n°CCNM/GF/COMP/WD(2002)7

[8] UNCTAD, “ Voluntary Peer Review on competition policy: Kenya” (2005), UNCTAD/DITC/CLP/2005/6

[9] MM de Fays, “ UNCTAD peer review mechanism for competition law : 10 years of existence – A comparative analysis of the implementation of the Peer Review’s recommendations across several assessed countries” (2015)

[10] Burundi Investment Promotion Authority “Burundi at a Glance – Legal and political structure”, http://www.investburundi.com/en/legal-structure

[11] Africa Time, “Loi sur la concurrence : 4 ans après, elle n’est pas encore appliquée” (Competition Law : 4 years after, it is still not implemented) (2014), http://fr.africatime.com/burundi/articles/loi-sur-la-concurrence-4-ans-apres-elle-nest-pas-encore-appliquee