What is Merger?

Most mergers pose little or no serious threat to competition, and may actually be pro-competitive. Such benevolent mergers have a number of economic advantages such as resultant economies of scale, reduction in the cost of production and sale, and gains of horizontal integration. There could also be more convenient and reliable supply of input materials and reduction of overheads. These advantages could, and should, lead to lower prices to the consumer.

Other mergers, however, may harm competition by increasing the probability of exercise of market power and abuse of dominance. Mergers can also sometimes produce market structures that are anti-competitive in the sense of making it easier for a group of firms to cartelise a market, or enabling the merged entity to act more like a monopolist.

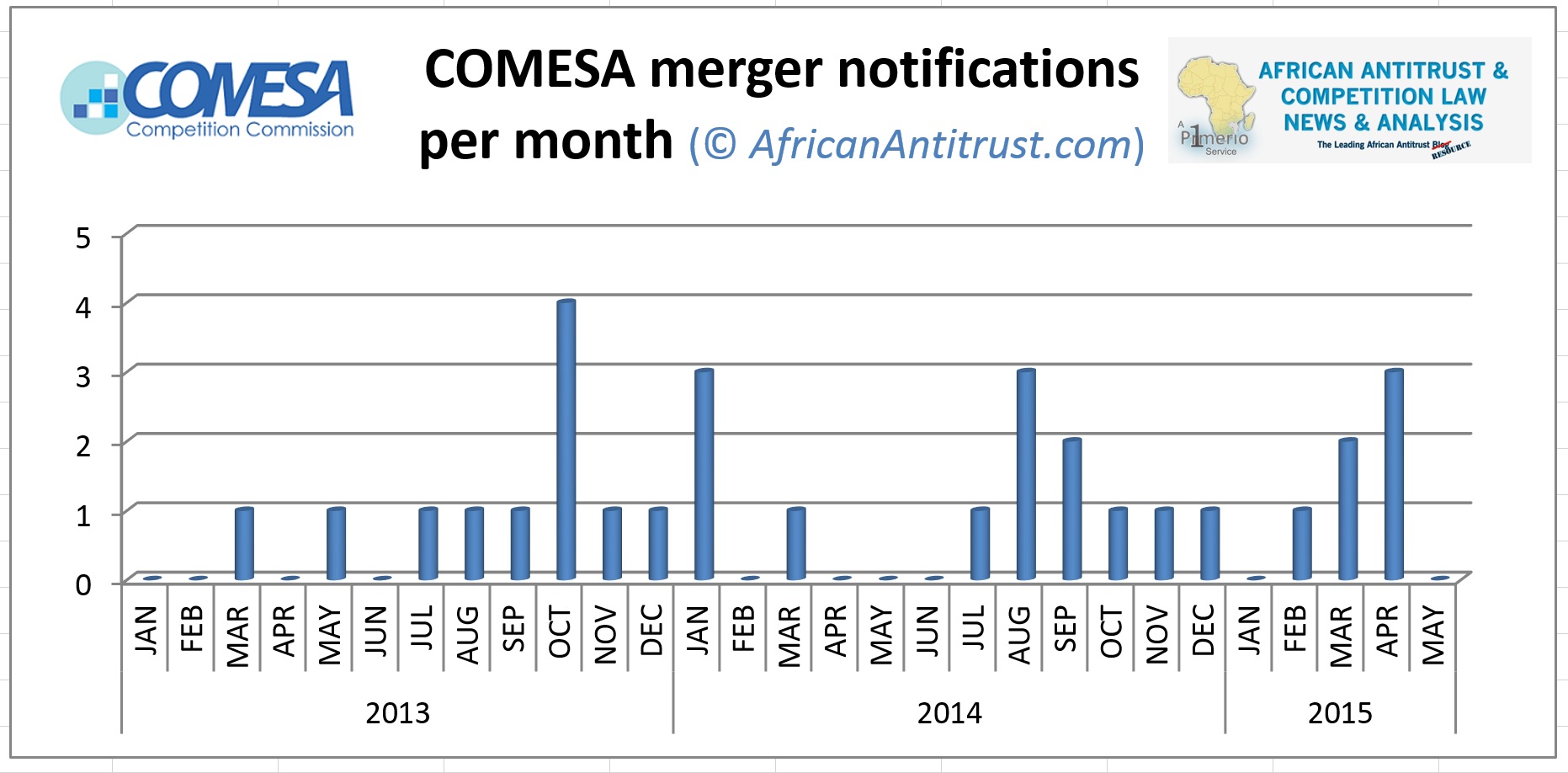

An increasing number of business firms in the COMESA region are merging, or entering into other forms of strategic alliances, in order to take advantage of the many economic benefits that arise from such transactions. Undertakings in the COMESA region are relatively small compared with those in other parts of the world. Mergers in the region, however, would create ‘regional champions’ capable of competing with other international companies on an equal footing.

Companies however need to notify the Commission their proposed mergers to enable the mergers to be thoroughly examined for any anti-competitive features that might reduce or eliminate the transaction’s economic benefits. Not all mergers are notified to the Commission. Only those large mergers that exceed a certain prescribed threshold have to be notified. The fee for notifying mergers is not punitive, but is only meant to defray the costs to the Commission for examining the transactions. The COMESA Competition Rules provide for a relatively small merger notification fee calculated at 0.01% of the combined annual turnover or combined value of assets in the COMESA region of the merging parties. (NOTE by editor: The CCC has, as of 5 Nov. 2014, changed this incorrect statement and deleted all references to filing fees entirely.) Failure to notify mergers can however be very costly to the merging parties. The Regulations provide for a high penalty of up to 1% of the merging parties’ annual turnover in the COMESA region for not notifying eligible mergers

Merger in COMESA Competition Regulations

The word merger in this COMESA Competition Regulation is construed in the context of its definition under Article 23(1) of the Regulations.

Control is used in the context of controlling interest as defined under Article 23(2) of the Regulations. Without prejudice to Article 23(2), control shall be constituted by rights, contracts or any other means which, either separately or in combination with and having regard to the considerations of fact or law involved, confer the possibility of exercising decisive influence on an undertaking. The COMESA Competition Commission (‘the Commission’) shall deem a person or undertaking to exercise control within the meaning of Article 23(2) of the Regulations if the person or undertaking;

- Beneficially owns more than one half of the issued share capital of the undertaking;

- Is entitled to cast a majority of the votes that may be cast at a general meeting of the undertaking, or has the ability to control the voting of a majority of those votes that may be cast at a general meeting of the undertaking, or has the ability to control the voting of a majority of those votes, either directly or through a controlled entity of the undertaking;

- Is able to appoint, or to veto the appointment, of a majority of the directors of the undertakings;

- Is a holding company, and the undertaking is a subsidiary of that holding company;

- In the case of the undertaking being a trust, has the ability to control the majority of the votes of the trustees or to appoint or change the majority of the beneficiaries of the trust;

- In the case of an undertaking being a close corporation, owns the majority of the members’ interest or controls directly, or has the right to control, the majority of the members’ votes in the close corporation; or

- Has the ability to materially influence the policy of the undertaking in a manner comparable to a person who, in ordinary commercial practice, can exercise an element of control referred to in paragraphs (a) to (f).

The Commission shall assess material influence on a case by case basis, having regard to the overall relationship between the acquiring firm and the target firm in light of the commercial context.

In its assessment of material influence, the Commission shall focus on the acquiring undertaking(s). Minority and other interests shall be examined by the Commission to the extent that they are able to influence the policy of the undertaking(s) concerned.

The Commission shall consider an acquiring firm’s ability to influence policy relevant to the behaviour of the target firm in the market place. This includes the management of the business, in particular in relation to its competitive conduct, and thus includes the strategic direction of a firm and its ability to define and achieve its commercial objectives.

The Commission shall consider an acquiring firm’s ability to block special resolutions by virtue of share ownership or other factors, including:

- The distribution and holders of the remaining shares, in particular whether the acquiring entity’s shareholding makes it the largest shareholder;

- Patterns of attendance and voting at recent shareholders’ meetings based on recent shareholder returns, and, in particular, whether voter attendance is such that in practice a minority holder is able to block a special resolution;

- Any special voting or veto rights attached to the shareholding under consideration; and

- Any other special provisions in the constitution of the target firm which confer the ability to exercise influence.

Where an acquiring firm is not able to block special resolutions of the target firm, the Commission shall have regard to the status and expertise of the acquiring firm, and its corresponding influence with other shareholders, and shall consider whether, given the identity and corporate policy of the target company, the acquiring firm may be able to exert material influence on policy formulation at an earlier stage.

The Commission shall review the proportion of Board of Directors appointed by the acquiring firm and the corporate/industry expertise of members of the Board appointed by the acquiring firm. The Commission may also assess the identities, relevant expertise and incentives of other Board Members.

Interpretation of Article 23(3) of the COMESA Competition Regulations

Article 23(3) of the COMESA Competition Regulations (‘the Regulations’) provides that:

“This Article shall apply where:

-

both the acquiring firm and target firm or either the acquiring firm or target firm operate in two or more Member States; and

-

the threshold of combined annual turnover or assets provided for in paragraph 4 is exceeded”.

The interpretation shall focus on Article 23(3)(a) since Article 23(3)(b) is superfluous due to the non-existent of thresholds currently. Article 23(3)(a) is divided into two parts as follows:

- both the acquiring firm and the target firm operate in two or more Member States;

- either the acquiring firm or target firm operate in two or more Member States.

The meaning of the first part above is that for a merger to fall within the dominion of Part IV of the Regulations is that both the acquiring firm and the target firm should operate in two or more Member States. For example if Company A is the acquiring firm and it operates in Zambia and Malawi and Company B is the target company and it equally operates in Zambia and Malawi, then the requirements of the first limb are satisfied and the merger falls within the ambit of Part IV of the Regulations.

Another scenario where the first part is satisfied is where Company A the acquiring firm operates in Zambia and Malawi and Company B the target firm operates in Zambia and Ethiopia. In this example, both Company A and Company B operate in two or more Member States.

The third scenario where the first part is satisfied is where Company A the acquiring firm operates in Zambia and Malawi and Company B the target firm operates in Djibouti and Madagascar. In this example, both Company A and Company B operate in two or more Member States.

As regards the second part, a merger falls within the province of Part IV of the Regulations where for example Company A the acquiring firm operates in Kenya and Seychelles and acquires Company B the target which has no operations in the COMESA Member States.

Another scenario where the second part is satisfied is where Company A the acquiring firm has no operations in any of the COMESA Member States but acquires Company B the target which operates in Rwanda and Burundi.

The foregoing are pursuant to the second limb which uses the words “either or” and therefore presupposes that both the acquiring firm and the target firm do not have to operate in two or more Member States as is the case for the first limb but that where either the target or acquiring is operates in two or more Member States, the merger is captured under Part IV of the Regulations.

It is important to note that where the acquiring firm operates in only one Member State and the target firm operates in another Member State and only that Member State, then such a merger does not satisfy the jurisdictional requirements of Part IV of the Regulations. This is however on the premise that such firms do not control any other firm whether directly or indirectly in a third Member State. Such firms should also not be controlled whether directly or indirectly by any other firm in a third Member State. For example, where Company A the acquiring firm operates in Swaziland only and Company B the target operates in Rwanda only, such a merger does not meet the jurisdictional requirements of Part IV of the Regulations. The situation may be different where Company A has a stake in Company C which operates in Mauritius or Company B has a stake in Company D which operates in the Democratic Republic of Congo.

The word operate is taken to mean that a firm(s) in issue derives turnover in two or more Member States. Therefore does not need to be directly domiciled in a Member State but it can have operations through exports, imports, subsidiaries etc. in a Member State.

re Group Proprietary Limited and Joint Medical Holdings Limited had entered into a consent agreement with record-breaking consequences. The two hospital groups admitted to not complying with the Competition Act, 1998 (“the Act”) by failing to notify the competition authorities of their merger and to obtain the required approval prior to the merger being implemented; and subsequently agreed to jointly pay an administrative penalty of 10 million Rand, or approximately U.S. $690,000. (Interestingly, the parties also conceded that they were guilty of fixing the price of services back in 2004 but the Tribunal dropped these charges.)

re Group Proprietary Limited and Joint Medical Holdings Limited had entered into a consent agreement with record-breaking consequences. The two hospital groups admitted to not complying with the Competition Act, 1998 (“the Act”) by failing to notify the competition authorities of their merger and to obtain the required approval prior to the merger being implemented; and subsequently agreed to jointly pay an administrative penalty of 10 million Rand, or approximately U.S. $690,000. (Interestingly, the parties also conceded that they were guilty of fixing the price of services back in 2004 but the Tribunal dropped these charges.) The R10-million administrative penalty is a record amount for gun-jumping, or the failure to notify the competition authorities of a merger. Previously, the highest penalty for a failure to notify was just over R1-million. The new record penalty follows numerous warnings by the Competition Commission (“Commission”) that it intended to materially increase penalties for failure to notify mergers — says Andreas Stargard, an antitrust practitioner with Pr1merio advisors, “South Africa has a suspensory merger-notification system, like most international antitrust regimes do. And unlike other African countries, such as Senegal or Mauritius, the domestic S.A. competition legislation prohibits transacting parties from effecting the transfer of control or beneficial ownership prior to obtaining clearance from the authorities.”

The R10-million administrative penalty is a record amount for gun-jumping, or the failure to notify the competition authorities of a merger. Previously, the highest penalty for a failure to notify was just over R1-million. The new record penalty follows numerous warnings by the Competition Commission (“Commission”) that it intended to materially increase penalties for failure to notify mergers — says Andreas Stargard, an antitrust practitioner with Pr1merio advisors, “South Africa has a suspensory merger-notification system, like most international antitrust regimes do. And unlike other African countries, such as Senegal or Mauritius, the domestic S.A. competition legislation prohibits transacting parties from effecting the transfer of control or beneficial ownership prior to obtaining clearance from the authorities.”