Retail antitrust: “mushrooming” shopping malls vs. SMEs, and possible cartel follow-on enforcement on the horizon for CCC

As reported in the Swazi Observer and other news outlets, the COMESA Competition Commission (“CCC”) recently expressed an interest in investigating the effect that larger shopping malls have had on competition in the common market’s retail sector.

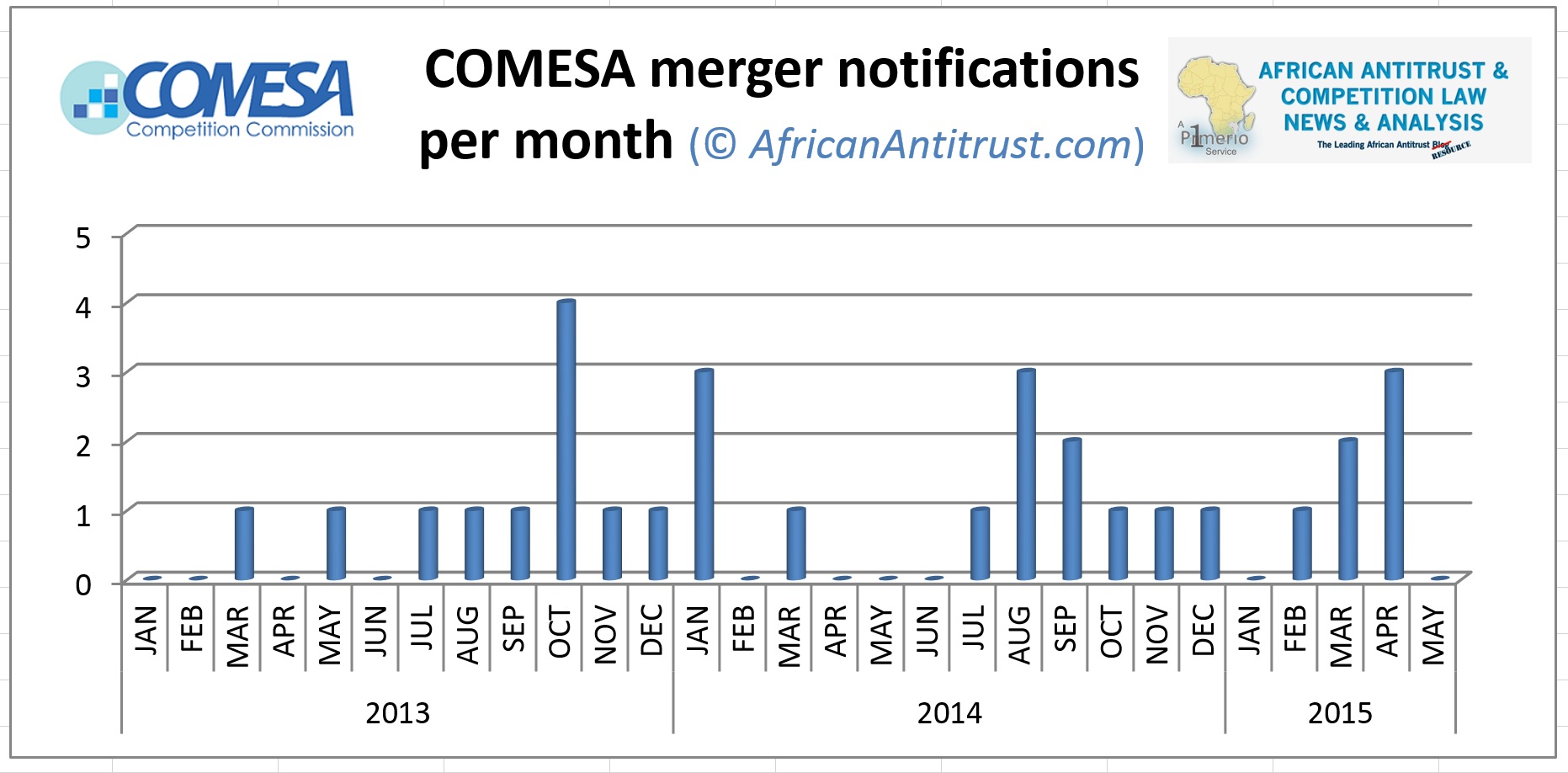

This is one of the first non-M&A investigations undertaken by the CCC, according to a review of public sources. While observers in the competition-law community have witnessed several merger notifications (and clearances) under COMESA jurisdiction, there has been no conduct enforcement by the young CCC to speak of. Indeed, CCC executive director George Lipimile stated at a conference in November 2014: “Since we commenced operations in January, 2013 the most active provisions of the Regulations has been the merger control provisions.” Andreas Stargard, an attorney with the boutique Africa consultancy Pr1merio, notes:

“Looking at the relative absence of enforcement against non-merger conduct (such as monopolisation, unilateral exclusionary practices, cartels, information exchanges among competitors or other conduct investigations), this new ‘shopping mall sectoral inquiry‘ may thus mark the first time the CCC has become active in the non-merger arena — a development worth following closely. Moreover, the head of the CCC also announced future enforcement action against cartels, albeit only those previously uncovered in other jurisdictions such as South Africa, it appears from his prepared remarks.”

The CCC’s interest in the mall sector was revealed during one of the agency’s “regional sensitisation workshops” for business journalists (AAT previously reported on one of them here). At the event, Lipimile is quoted as follows:

“The little shops in the locations seem to be slowly disappearing because everybody is going into shopping malls. And these shopping malls and the shops in them are mostly owned by foreigners.”

The investigation will take a sampling from the economies of several of the 19 COMESA member states and attempt to determine whether the “mushrooming” growth of shopping malls negatively affects local small and medium enterprises in the whole common market.

Rajeev Hasnah, a Pr1merio consultant, former Commissioner of the CCC and previously Chief Economist & Deputy Executive Director of the Competition Commission of Mauritius, commented that,

“Conducting market studies is one of the functions of the CCC and it is indeed commendable that the institution would contemplate on conducting such a study in the development of shopping malls across the COMESA region. I believe that this will then enable the institution to correctly identify and appreciate the competition dynamics in the operations of shopping malls and the impact they have on the economy in general. The study should also identify whether there are areas of concerns where the CCC could initiate investigations to enable competition to flourish to the benefit of businesses, consumers and the economy in general. We look forward to the undertaking of such a study and its findings.”

AAT agrees with this view and welcomes the notion of the CCC commencing substantive non-merger investigations. We observe, however, that the initial reported statements on the part of the CCC tend to show that there is the potential for dangerous local protectionist motives to enter into the legal competition analysis. As Mr. Lipimile stated at the conference:

“Though [the building of malls] might be seen as a good thing, it may negatively impact on our local entrepreneurship and might lead to poverty. Before shopping malls were built, local entrepreneurs realised sales from their products. Now malls are taking over. … [A] strong competition policy can be an effective tool to promote social inclusion and reduce inequalities as it tends to open up more affordable options for consumers, acting as an automatic stabiliser for prices”

That said, Mr. Lipimile also stated at the same event, quite astutely, that a “solid competition framework provides a catalyst to increase productivity as it generates the right incentives to attract the most efficient firms.” In the rational view of antitrust law & economics, if — after an objective review such as the study announced by the CCC — the “most efficient” firm happens to be a larger shopping mall that does not otherwise foreclose equally effective competition, then the Darwinian survival of the fittest in a market economy must not be impeded by regulatory intervention.

Mr. Lipimile himself seemed to agree in November 2014, when he said that the 19-member COMESA jurisdiction must have regard to “its trading partners [which] go beyond the Common Market hence, it requires consensus building and a balancing act.” At this time, “when regional integration is occupying the centre stage as one of the key economic strategies and a rallying point for the development of the African continent,” domestic protectionist strategies have no place in antitrust & competition law. Said Mr. Lipimile: “[R]egional integration can only be realized by supporting a strong competition culture in the Common Market,” which would not support a more reactionary, closed tactic of a regulatory propping-up of “domestic champions” versus more efficient foreign competition. As the CCC head recognised, “[t]he purpose of competition law is to facilitate competitive markets, so as to promote economic efficiency, thereby generate lower prices, increase choice and economic growth and thus enhance the welfare of the general community.”