South African Antitrust Developments: a WRAP from the Comp-Corner

Issue 1 – May 2016

The editors and authors at AAT welcome you to our new semi-serial publication: “The WRAP.” In this first WRAP edition, we look back over recent months and provide an overview of the key recent developments which antitrust practitioners and businesses alike should take note of in respect of merger control and competition law enforcement.

As always, thank you for reading the WRAP, and remember to visit AAT for up-to-date competition-law news from the African continent.

–Ed. (we wish to thank our contributors, especially Michael Currie, for their support)

Price-fixing in Kenya is prohibited under the Competition Act No. 12 of 2010 under Section 21 (3) (a) which provides that any agreements, decisions or concerted practices which directly or indirectly fix purchase or selling prices or any other trading condition is prohibited under the Act, unless they are exempt in accordance with the provisions of Section D of Part III.

Part III B further prohibits price-fixing by trade associations under Section 22 (b) (i) which provides that the making, indirectly or directly, of a recommendation by a trade association to its members or to any class of its members which relates to the prices charged, or to be charged by such members, or to any class of members, or to the margins included in the prices, or to the pricing formula used in the calculation of those prices, constitutes a restrictive trade practice under the Act.

Section 29 (1) of the Act further outlines the rules for exemptions in respect of professional associations. It provides that a professional association whose rules contain a restriction that has the effect of preventing, distorting or lessening competition in a market must apply in writing or in the prescribed manner to the Competition Authority for an exemption. Sub-section (2) goes on to explain what factors the Authority considers in order to grant an exemption for a specified period. These include:

Maintenance of professional standards

Maintenance of the ordinary functioning of the profession

Internationally applied norms

Section 29 (5) further gives discretion to the Authority to revoke an exemption in respect of such rules or the relevant part of the rules, at any time, if the Authority considers that any rules, either wholly or in part, should no longer be exempt under this section. For instance, if they no longer promote consumer welfare or do not enhance standards in the profession.

Price setting concerns by Law Society of Kenya, LSK

Professional fees for advocates in Kenya are set by the Chief Justice under the Advocates Act Chapter 16 of the Laws of Kenya. Part IX Section 44 provides that the Chief Justice may by order prescribe and regulate in such manner as he/she thinks fit the remuneration of advocates in respect of all professional business, whether contentious or non-contentious. Sub-section (2) also provides that the Chief Justice may prescribe a scale of rates of commission or percentage in respect of non-contentious business.

However, Section 45 provides that agreements in respect of remuneration may be made between the advocate and the client subject to permissible professional rules under section 46 of the Act. Therefore, as much as the Chief Justice may set professional fees under the Act, there is an opportunity for the advocate and the client to agree on professional fees subject to the Act. Moreover, a client has redress to apply to the courts under Section 45 (2) to set aside or vary such an agreement on grounds that it is harsh, unconscionable, exorbitant or unreasonable according to professional practice. The decision of the court on this matter is final.

The Chief Justice periodically revises the Advocates Remuneration Order which sets out the scale of professional legal fees. In doing so the Chief Justice considers factors such as inflation and the costs of providing legal fees. The Kenyan Advocates Remuneration Order was last revised upwards in 2014, increasing professional fees by 50%. The Order was last revised in 1997. Advocates had petitioned the Chief Justice to do so in order to enable them cope with tough economic conditions. Recently there was a public discourse on whether advocates should have set fees. Stakeholders argue that the Chief Justice’s decision to adjust fees may not be entirely objective because since he or she has qualifications in law, and could revert to the profession upon retirement from office.

LSK on the other had contends that the minimum fees help protect consumers from poor services, and it reduces the price wars that would occur without the scale of fees. Under the Advocates Act, charging below the set scale of fees amounts to undercutting. This is a professional offense that could result in the concerned advocate being suspended or struck off the roll. Moreover, any agreements or instruments prepared by the concerned advocate are liable to be invalidated by the courts.

The question arose among legal stakeholders as to whether the Authority could intervene in relation to the scale of professional fees under the provisions on price-fixing. The LSK chairperson recently commented that it is beyond the jurisdiction of the Authority, as the Remuneration Order seeks to set minimum fees and not a fixed rate. However, it is clear from the provisions of Section 29 that any professional body whose rules, having regard to internationally applied standards, contain any restrictions which have the effect of preventing or substantially lessening competition in a market, must apply to the Competition Authority for an exemption of the said rules.

Price Setting Concerns by Association of Kenya Reinsurers, AKR

The Association of Kenya Reinsurers is regulated by the Kenya Reinsurance Corporation Limited Act, Cap 487A of the Laws of Kenya. The Association consists of the following companies: Kenya Reinsurance Corporation Limited, Africa Reinsurance Corporation Limited, East Africa Reinsurance Company, Zep – Re and Continental Reinsurance Limited. The Authority recently investigated this association for price fixing following a complaint lodged from the National Intelligence Service (NIS). The association, through a circular dated 2, October 2013, had advised its members on the minimum applicable premiums upon renewal of NIS Group Life Scheme for 2013/2014. Insurance companies are required by their regulator Insurance Regulatory Authority (IRA) to use an independent actuary to come up with their own individual premium rates, which they file with the IRA for approval.

The association is required under the Competition Act Section 29 (1) to apply in the prescribed manner to the Authority for an exemption in relation to any anti-competitive rules. Section 22 (2) (b) also prohibits the making, directly or indirectly, of a recommendation by a trade association to its members, or to any class of its members which relates to the prices charged, or to be charged by such members, or any such class of members, or to the margins included in the prices, or to the prices, or to the pricing formula used in the calculation of those prices. Therefore, the Association is legally bound to seek the approval of the Authority in order to set a minimum fee for any particular group of consumers. Moreover, the association may be in violation of Section 21 (f) of the Competition Act which prohibits any decisions by associations of undertakings which applies dissimilar conditions to equivalent transactions with other trading parties, thereby placing them at a competitive disadvantage, unless they are exempt in accordance with the provisions of Section D of Part III.

Conclusion

In conclusion, professional associations in Kenya should take advantage of the provisions of Section 29 of the Competition Act which allow professional associations to apply rules whose effect is the lessening of competition in the market, provided they are applied to enhance professional standards, the ordinary functioning of the profession or internationally applied norms for the benefit of consumers.

Price-fixers face up to 10 years prison time, starting May 1st

Prison time for executives is now firmly on the not-so-distant horizon in South Africa: As reported in some media outlets, the criminalisation of certain hard-core (and possibly lesser) antitrust offences is finally being implemented in the Republic — notably after more than 8 years of the relevant legislation technically being on the books.

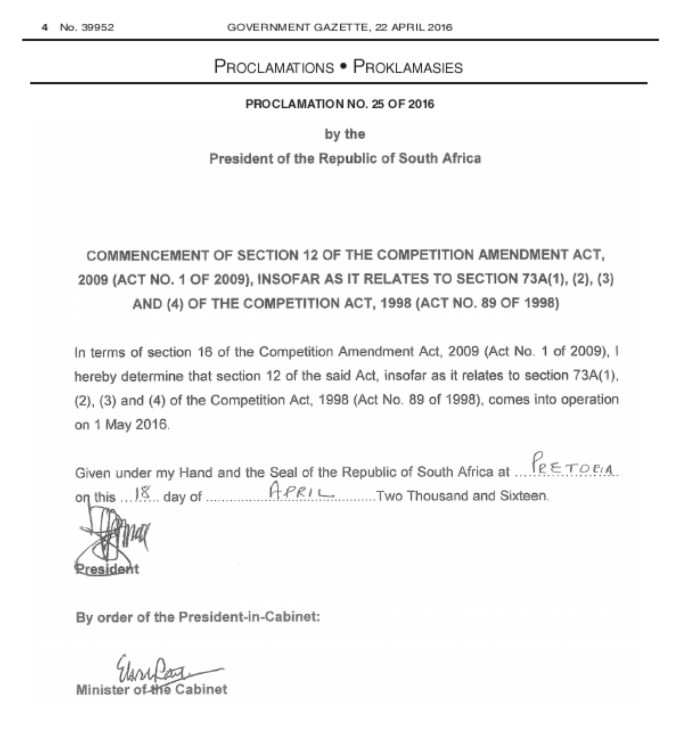

We are referring to the “phased” implementation of the 2009 Competition Amendment Act. The legislation technically criminalised hard-core antitrust offences such as bid-rigging or price-fixing cartels. However, President Zuma has, until now, not yet implemented or effectively signed the criminal provision of the Act (section 73A) into law.

Enter his Economic Development Minister,Ebrahim Patel:

According to news reports, Mr. Patel announced today (Thursday), that the criminalisation of the price-fixing cartel offence would henceforth be enforced. Section 73A will be gazetted tomorrow, 22 April 2016, and hold the force of law from 1 May 2016. BDLive also reports that even the lesser “abuse of dominance” (or more commonly “monopolisation”) offence would be subject to the criminal penalties, but AAT is awaiting independent confirmation on this subject. As Andreas Stargard, a U.S.-based Pr1merioantitrust practitioner with a focus on Africa and experience counseling clients in criminal competition matters, explains:

“If Mr. Patel indeed made this statement, and I doubt this, it would signal a departure from the rest of the world’s antitrust regimes: It is highly uncommon to have the monopolisation offence constitute a criminal act — indeed I am aware of no jurisdiction where this is the case.

In the United States, the only conduct constituting a Sherman Act offence pursued by the DOJ as a potential felony involve so-called ‘hard-core’ violations. This would include horizontal price-fixing among competitors; territorial allocations; output allocations; and bid-rigging. The same holds true in the UK. That said, monopolisation or abuse of dominance is simply not among the criminalised antitrust violations elsewhere, and I’d be surprised if South Africa took this unusual path.“

We have since been able to confirm that the BDLive report incorrectly refers to abuse of dominance as being criminalised. AAT has obtained a copy of Mr Patel’s speech which provides clearly only for cartel conduct to be subjected to imprisonment:

“We are confident that because our work on cartels over the past five years has given clarity in the market on what collusion entails and what kind of acts falls within prohibited practices, we can now step up our efforts to the next level in our endeavor to combat corruption, cartels and anti-competitive conduct that raise prices and keep businesses and new entrants out of local markets.

Accordingly, government will tomorrow gazette a Presidential Proclamation that brings into effect certain sections of the Competition Amendment Act, with effect from 1 May 2016, which make it a criminal offence for directors or managers of a firm to collude with their competitors to fix prices, divide markets among themselves or collude in tenders or to acquiesce in collusion and they expose themselves to time in jail if convicted.”

The Patel announcements come ahead of his upcoming budget vote speech, and as he has shown in recent months, Mr. Patel is a proud advocate for tougher competition enforcement in the country. “We want to make sure that it just does not make sense to collude,” he is reported as saying today. This follows the Minister’s speech during the Parliament debate in February, where he announced that, “we will now introduce measures shortly to make it a criminal offence in any industry to collude and fix-prices. It will send a message to everyone that we mean business on stamping out corruption and collusion. We must build competitive strengths through innovation, not through sitting in rooms somewhere fixing tenders, prices and contracts.”

White-collar crime: it pays, but is getting riskier

We live in the era of the PanamaPapers, where the notion of white-collar business people going to jail is not an entirely unlikely outcome for some. Antitrust offences, however, have historically not been enforced worldwide as stringently as public corruption or tax-evasion matters, for instance. Key jurisdictions with criminalisation of competition offences remain few, notably the U.S. and the UK.

In South Africa, since at least 2014, both Competition Commissioner Tembinkosi Bonakele and Minister Patel have been engaging in discussions on how and when to implement the Act “to ensure that the necessary institutional capacity is available to apply the [criminal] amendments.” While some provisions (relating to the agency’s market-inquiry powers) went into effect in 2013, the criminalisation provisions remain unimplemented to date — but this is about to change.

During these negotiations, as reported on AAT, the minister and SACC admitted in a remarkable self-assessment that the Commission then lacked “the institutional capacity needed to comply with the higher burden of proof in criminal cases.” One notable aspect of potential discord lies in not only in the different standard of proof in civil vs. criminal matters (“more probable than not” vs. “beyond a reasonable doubt”), but perhaps more importantly can be found on the procedural side, preventing rapid implementation of the law: There has been historic friction between various elements of the RSA’s police forces and (special) prosecutorial services, and the power to prosecute crimes notably remains within the hands of the National Prosecuting Authority, supported in its investigations by the South African Police Service.

History & Legislative Background – and a bit of Advice from the U.S.

Starting in the spring and summer of 2008, the rumoured legislative clamp-down on corrupt & anti-competitive business practices by the government made the RSA business papers’ headlines.

During a presentation Mr. Stargard gave at a Johannesburg conference in September that year (“Criminalising Competition Law: A New Era of ‘Antitrust with Teeth’ in South Africa? Lessons Learned from the U.S. Perspective“), he quoted a few highlights among them, such as “Competition Bill to Pave Way for Criminal Liability”, “Tough on directors”, “Criminalisation of directors by far most controversial”, “Bosses Must Pay Fines Themselves”, “Likely to give rise to constitutional challenges”, and “Disqualification from directorships … very career limiting”.

Stargard, whose practice includes criminal and civil antitrust work, having represented South African Airways in the global “Air Cargo Cartel” investigations, also notes that international best-practice recommendations all highlight the positive effect of criminal antitrust penalties. For example, the OECD’s Hard-Core Cartel Report recommended that governments consider the introduction and imposition of criminal antitrust sanctions against individuals to enhance deterrence and incentives to cooperate through leniency programmes. Then-DOJ antitrust chief Tom Barnett said in 2008, the year South Africa introduced its legislation: “Jail time creates the most effective, necessary deterrent. … [N]othing in our enforcement arsenal has as great a deterrent as the threat of substantial jail time in a United States prison, either as a result of a criminal trial or a guilty plea.”

Mr. Stargard points out the following recommendations to serve as guide-posts for the Commission going forward in its “new era” of criminal enforcement:

Cornerstones of a successful criminal antitrust regime

Crystal-clear demarcation of criminal vs. civil conduct

Highly effective leniency policy also applies to individuals

Standard of proof must be met beyond a reasonable doubt

No blanket liability for negligent directors – only actors liable

Plea bargaining to be used as an effective tool to reduce sentence

Clear pronouncements by enforcement agency to help counsel predict outcomes

What lies ahead?

After 1 May, the penalties for violating Section 73A of the Competition Amendment Act will range from a period of up to 10 years in prison and/or a fine of up to R500 000.00. It appears that the introduction of criminal provisions will not have a retrospective effect, but will only apply prospectively from 1 May 2016 onward.

Robber barons…

The introduction of criminal sanctions for cartel conduct raise several constitutional concerns. It is likely that, in the event of the imposition of criminal sanctions, the constitutional validity of the relevant Competition Amendment Act provisions will be challenged. In particular, section 73A(5) of the Amendment Act, introduces a reverse onus on the accused, in that the onus for rebutting the Competition Tribunal of Competition Appeal Court’s conclusion rests with the accused in criminal proceedings. The reverse onus’ constitutional validity is questionable given the constitutional right to a fair trial and the right to be presumed innocent.

John Oxenham, also with Pr1merio, notes that the “criminalisation of cartel conduct is a development which needs to be carefully considered and well planned before its official introduction due to the imminent effects it will have on current South African competition law.” The successful prosecution of cartel conduct rests heavily on the efficiency of corporate leniency policies. The introduction of criminal sanctions and in turn the National Prosecuting Authority will undoubtedly have an effect on the current corporate leniency policies. It is important to consider granting the staff of a company applying for corporate leniency in relation to cartel activity ‘full immunity’ from criminal prosecution in order to encourage companies to come forward and not debilitate the very purpose of corporate leniency policies. The careful integration of criminal sanctions is therefore vital in ensuring that the very purpose of its introduction, namely to deter corruption and anti-competitive conduct, is achieved.

Update [22 April 2016]: As anticipated, the South African government gazetted [published] the official document starting the era of criminal antitrust enforcement under section 73A as of today, signed 18 April 2016:

“Partisanship can degrade the brand of the antitrust agencies, reduce their influence aboard, and discourage longer term investments that strengthen agency performance. Though difficult to quantify, these constitute a potentially serious, unnecessary drag on agency effectiveness”

(William Kovacic, “Policies and Partisanship in U.S. Federal Antitrust Enforcement” (2014) Antitrust Law Journal, Vol. 79 at 704).

In their article entitled “Developments in South African Merger Control – Ministerial Interventionism and the Impact on Timing & Certainty,” John Oxenham, Andreas Stargard, and Michael Currie argue that, while the existence of ‘public-interest’ provisions in merger control is an express feature in certain jurisdictions’ antitrust regimes, the manner and regularity with which they are applied remains a significant challenge both for antitrust practitioners and for their clients gauging certainty of their foreign investments.

A consideration of the developments in the South African context indicates the substantial risks associated with the manner in which antitrust agencies and governmental departments approach public interest considerations in merger proceedings.

Merging firms, particularly multinationals, need to be acutely aware of the challenges and risks associated with the use of public-interest considerations throughout merger-control proceedings in South Africa. Recent interventionist strategies have had a significant impact on two key features: the timing and cost of concluding mergers in the region.

The paper was presented at this year’s ABA Antitrust Spring Meeting, the largest competition-law focussed conference in the world, taking place annually in Washington, D.C. AAT’s readers have exclusive free access to the PDF here.

Key competition-law conference features dedicated panel discussion on African antitrust developments

By Michael-James Currie

The 54th annual American Bar Association Antitrust Spring Meeting was held in Washington, D.C., during the second week of April 2016 and the AAT editors were there to ensure that we provide our readers with an update on the latest developments in relation to African antitrust issues, discussed during a panel held last Friday.

ABA Africa Panelists

Given that mergers hit a global all-time high last year with the total value of transactions amounting to over USD 4.6 trillion, merger control is certainly at the forefront of many antitrust practitioners. The interest in mergers and acquisitions has perhaps gained even further attention in light of the announcement this week that the USD160 billion Pfizer/Allergan global mega-deal has been officially abandoned, despite the transaction having already been filed before all the relevant competition agencies around the world. While the Pfizer/Allergan deal was called off as a result of new tax laws and therefore not as a result of antitrust issues directly, the deal did put multinational mega-deals firmly in the spotlight.

The Pfizer/Allergan deal is not the only mega-deal that faced significant government opposition. It was announced this week that Halliburton’s takeover of Baker Hughes, in a deal valued at USD 25 billion, is going to be strongly opposed by the U.S. DOJ.

It is, however, not only the U.S. Government that is having a significant impact on multinational deals, as evidenced by the Anbang Insurance and Starwood Hotels & Resorts deal, valued at USD 14 billion, which has also been abandoned after mounting pressure by the Chinese government.

From an African perspective, the South African Competition Commission just last week extended its investigation in the USD 104 billion SABMiller and Anheuser-Busch InBev merger. It is widely suspected that the request for the extension is due to intervention by the Minister of Economic Development, in relation to public interest grounds. Although there is no suggestion at this stage that Minister Patel is opposing the deal, the proposed intervention does highlight bring into sharp focus the fact that multinational mega-deals face a number of hurdles in getting the deal done.

‘Getting multinational deals through’ is a hot topic at the moment amongst antitrust practitioners and is and the ABA thought it beneficial to have a panel discussion dedicated purely to merger control issues across African jurisdictions. In particular, the panel addressed some of the key issues which merging parties need to consider, including inter alia issues relating to harmonisation across agencies, the role of public interest considerations, prior implementation and the need for upfront substantive economic assessments.

The panel consisted of a varied mix of panellists from both private practice and government, and included Pr1merio director John Oxenham (he is also a founding partner at South African based law firm Nortons Inc.), economist and former Commissioner of the COMESA Competition Commission (COMESA CC) Rajeev Hasnah (Rajeev was also a former commissioner of the Mauritius Competition Commission and is an economist for Pr1merio), manager of the South African Competition Commission office, Wendy Ndlovu, and Kenyan based external counsel Anne Kiunuhe (Anne practices at the law firm Anjarwalla & Khanna).

The panellists were tasked with addressing a variety of topics: we summarise below some of the key issues which the panellists highlighted, which merging parties, practitioners and antitrust agencies themselves (amongst whom Tembikosi Bonakele, the South African Competition Commissioner was present in the panel audience) should be cognisant of in relation to merger control in Africa.

John Oxenham and Wendy Ndlovu at ABA Spring Meeting 2016 in Washington, D.C.

John Oxenham

John pointed out that from a South African perspective, mergers undergo a robust evaluation by the Competition Authorities and that although the investigation of most large mergers is completed within 60-70 days, the fact that the Commission may request the Competition Tribunal for an extension of up to 15 business days at a time, may result in the investigation of certain mergers taking considerably longer. The risk of a merger being delayed is increased significantly due to the level of third party interventionism, particularly ministerial intervention on public interest grounds.

John advised that merging parties should consider the impact that a particular merger will have on the public-interest grounds upfront to avoid delays in the investigation period as a result of further requests for information from the Commission, or may even amount to an incomplete filing.

In respect of substantive economic assessments, John pointed out that a number of jurisdictions, including South Africa, Namibia, Zambia and to a lesser extent Botswana, requires a substantive upfront economic assessment. In this regard the South African Competition Commission is perhaps the most robust in its economic evaluation of a merger in light of the resources dedicated to its own in-house economic department as well as utilising external experts when necessary. John also highlighted the fact that the South African Competition Authorities rely on oral testimony and expert witnesses are often subjected to substantial and lengthy examination and cross examination before the Competition Tribunal.

On the topic of gun-jumping or prior implementation, John mentioned that the following jurisdictions are examples of countries which do not require notification prior to implementing the transaction – in other words, they are not suspensory:

Malawi

Senegal

Mauritius

Whereas the following countries do require notification prior to implementation (suspensory merger control jurisdictions):

South Africa

Swaziland

Zambia

Botswana

On harmonisation, John confirmed that in relation to public interest considerations in merger control, the South African competition authorities play a leading role on the African continent and pointed out that in addition to Kenya and Tanzania, Namibia also considers public interest considerations and that there is a substantial amount of collaboration and information sharing between the South African and Namibian competition authorities, as was the case in the Walmart/Massmart deal.

Despite the information sharing between agencies, John confirmed that there are rules in place to protect confidential and legally privileged information and that the South African competition authorities are cognisant and respectful of these provisions.

Rajeev Hasnah

Rajeev Hasnah, Pr1merio economist and former COMESA Competition Commissioner, and Anne Kiunuhe from Kenya

Rajeev noted the significant progress which the COMESA CC has made in relation to merger control by publishing financial thresholds for mandatorily notifiable transactions and specified filing fees, as well as publishing guidelines which clarify when a merger will have a sufficient regional dimension to fall within the COMESA CC’s jurisdiction.

On the topic of harmonisation, Rajeev discussed the challenges due to a lack of harmonisation between COMESA and its member states and noted that COMESA does not have exclusive jurisdiction in the cases which do fall within its jurisdiction. Parties, therefore, may find themselves being required to file a merger both before the COMESA CC as well as before the respective national authorities. A further challenge facing the COMESA CC is that there are 19 member states and consequently, the relevant geographic market is significant. Accordingly, often the national authorities are best placed to evaluate a merger and will therefore defer the evaluation of the merger to the relevant national authority.

On the role of economic assessments, Rajeev stated that an economic assessment underlies any merger evaluation and that both the Mauritius Competition Commission and the COMESA Competition Commission conducts a comprehensive economic assessment of a merger.

Wendy Ndlovu

When asked on what role public interest considerations play in merger control in terms of the South African competition regime, Wendy indicated that the framework of the Competition Act specifically requires the competition authorities to consider the impact that a merger may have on the four specified public interest provisions contained in the Act. Wendy confirmed that an evaluation of public interest considerations may both justify a merger despite the merger likely being likely to cause a substantial lessening or prevention of competition in the market, alternatively, public interest considerations may lead to a prohibition or the imposition of conditions on a merger which raises no competition law concerns and may in fact be pro-competitive.

Wendy recognised that there is a need, however, for greater certainty in respect to the manner in which the South African authorities evaluate public interest considerations and pointed out that the Competition Commission is likely to finalise and publish its guidelines on the public interest assessment in an effort to promote greater certainty.

On prior the issue of prior implementation, Wendy pointed out that merging parties need to be mindful of the consequences of gun-jumping and noted that the South African Competition Tribunal has imposed administrative penalties, as in the Netcare case, on parties for failing to notify a mandatorily notifiable transaction.

Anne Kiunuhe

Anne discussed the Competition Authority of Kenya’s (CAK) willingness to focus not only on merger control but has also identified the CAK’s increasing tendency to investigate and prosecute firms engaged in restrictive practices (as demonstrated by the recent dawn raids conducted by the CAK in the fertiliser industry). Despite the CAK’s growing confidence, Anne pointed out that in respect of merger control, the CAK is open to and in fact often relies on precedent from foreign jurisdictions when evaluating a merger. In particular, Anne noted that public interest grounds are specifically considered during the merger review procedure and that in this respect, the CAK largely takes the lead from the South African competition authorities.

From a practical perspective, Anne mentioned that the CAK usually requests a meeting with the merging parties soon after a transaction has been notified, and that usually representatives from the merging parties, along with local external legal counsel, should be present. The CAK prefers that the representatives present should be the best placed to answer or address the CAK’s queries. This often necessitates representatives from the parent company being present as opposed to representatives from the subsidiary entities only.

The direct contact between the CAK and the merging parties is quite different from the manner in which the COMESA CC evaluates mergers where the consideration of a merger is done solely on the papers and any communication between the COMESA CC and the merging parties is done through the merging parties’ local external counsel.

As to legislative developments, Anne pointed out that the merger regulations in Kenya now provide that for purposes of establishing a “change of control”, it is sufficient if the acquiring firm is able to materially influence the commercial decisions of the target firm. Accordingly, the acquisition of a minority shareholding for instance may constitute a change of control if the holders of such shares may for instance exercise veto rights.

On COMESA, Anne mentioned that the COMESA CC permits merging parties to seek a comfort letter when unsure as to whether a merger requires filing and that the use of comfort letters has been rather prevalent.

Conclusion

The role of public interest considerations in merger control was a dominant focus point throughout the panel discussion due to this unique aspect in a growing number of African jurisdictions merger control provisions.

Please click on the following link to access a an article on the role of public interest considerations in merger control in South Africa, which addresses in particular, the impact of ministerial intervention in merger proceedings and the concomitant impact which such intervention has on the costs, timing and certainty of merger proceedings.

March 2016 has been a busy month for the competition agencies of South Africa and Kenya respectively. Both agencies carried out search and seizure operations as a result of alleged collusion within various sectors of the economy. While the March dawn raids are not connected, the South African Competition Authority, as part of its advocacy outreach, provided training to the Competition Authority of Kenya relating to inter alia, search and seizure operations.

South Africa

On 23 March 2016, the South African Competition Commission carried out search and seizure operations in the automotive glass fitment industry, as part of its continued investigation into alleged collusion within this sector.

Accordingy to the SACC, the raid was carried out “at the Gauteng premises of PG Glass, Glasfit, Shatterprufe and Digicall as part of its investigation of alleged collusion. PG Glass and Glasfit are automotive glass fitment and repair service providers; Shatterprufe supplies PG Glass and Glasfit with automotive glass while Digicall processes and administers automotive glass related insurance claims on behalf of PG Glass and Glasfit.”

John Oxenham, founding director of Pr1merio, notes that “[t]his most recent dawn raid follows on from those carried out towards the latter part of 2014 and 2015 and confirms that the SACC has adopted a more robust approach to investigating alleged anti-competitive practices.” In this regard, Commissioner, Tembinkosi Bonakele, confirmed at the 9th Annual Competition, Law, Economics and Policy Conference in November last year that the Competition Commission has in the past two years, “conducted more dawn raids than those conducted in preceding years since the Competition Commission came into existence” (nearly 16 years ago).

For an overview of dawn raids and cartel investigations in South Africa, please see the following GCR Article.

Kenya

This month the Competition Authority of Kenya (“CAK”) conducted its first dawn raid. The search and seizure operations were carried out in respect of two fertiliser firms, Mea Limited and the Yara East Africa, based on the CAK’s suspicion of price fixing occurring between these two firms, who together control approximately 60% of the fertiliser market. The CAK conducted the raid in accordance with Section 32 of the Competition Act, 2011 which provides for the Authority to enter any premises in which persons are believed to be in possession of relevant information and documents and inspect the premises and any goods, documents and records situated thereon. This follows an inquiry which was launched last year by Kenyan competition authorities into what the CAK termed “powerful trade associations exhibiting cartel-like behaviour specifically targeting banks, microfinance institutions, forex bureaus, capital markets as well as the agricultural and insurance lobbies”. The fact that the CAK has carried out its first dawn raid demonstrates its growing stature.

The fertiliser industry appears to be a priority sector for a number of African jurisdictions as the CAK’s investigation into this sector follows the South African Competition Commission’s investigation into the fertiliser industry (which resulted in a referral before to the South African Competition Tribunal for adjudication some years back). In this regard,the South African Competition Commission’s spokesperson stated that the “fertiliser sector is viewed as a priority sector, due to the its importance as an input in the agricultural sector” (as reported here on African antitrust)

Zambia

Interestingly, the Zambian Competition and Consumer Protection Commission (“CCPC”) had, in 2012, conducted dawn raids at the premises of two fertiliser companies, as a result of alleged collusion within the industry.

On a Path to Harmonisation?

While there are a number of practical and legislative hurdles to effectively carrying out cross border search and seizure operations, it appears that cross border investigations may not be too far off. This is particularly so as the various agencies within the Southern African Region have identified similar priority sectors (as evidenced by both the investigations into the fertiliser sectors as well as the various market inquiries into the grocery retail sector).

Uber Africa: Increased competitiveness not a boon for entrenched monopolies

Continuing our AAT multi-part series on innovation & antitrust we turn once again to the ubiquitous “Sharing Economy” we are witnessing not only in the United States and Europe but also on the African continent…

“The taxi industry is in the midst of a crisis. Once protected by a regulated monopoly of the commercial passenger motor vehicle transportation market, the industry now faces increasing competition from a new type of transportation service—ride-sharing. The emergence of companies like Uber, the most successful ride-sharing company, threatens to eliminate the taxi industry’s stronghold on the ground transportation market and possibly the industry itself.” (Erica Taschler, Institute for Consumer Antitrust Studies, in “A Crumbling Monopoly: The Rise of Uber and the Taxi Industry’s Struggle to Survive“)

Today, the Taxi Cab Association of Kenya announced protests against the “unfair competition” its members face from ride-sharing giant Uber, according to the organisation’s chairman, Josphat Olila. This is no news for folks in London, Brussels, Hamburg, or Washington — places where the taxi-medallion-capped brethren of Nairobi’s cabbies have all long ago gone through the protest phase against the rising tide of the “new economy’s” novel way of hailing cars. Examples abound, and all involve more or less refined antitrust arguments.

Andreas Stargard, an attorney with Africa competition advisors Primerio, sums it up as follows: “The pro-competitive notion of innovation-plus-price competition is perhaps best understood by looking at the views of two leading antitrust agencies, the FTC and the European Commission. Both have articulated simple and sound arguments for striking the right balance between regulatory limits for the protection of passengers, as well as allowing innovative technologies to enhance the competitive landscape and thereby increasing transportation options for riders. In antitrust law, more options usually equal better outcomes.”

U.S.

Here is what the U.S. Federal Trade Commission had to say in 2013 about the D.C. taxi commission’s ‘unfair competition’ argument against ride-sharing services:

“The staff comments recommend that DCTC avoid unwarranted regulatory restrictions on competition, and that any regulations should be no broader than necessary to address legitimate public safety and consumer protection concerns. … [T]he comments recommend that DCTC allow for flexibility and experimentation and avoid unnecessarily limiting how consumers can obtain taxis.”

Crucially, the Kenyan cabbies’ argument that Uber should be banned is based on price competition from Uber’s lower fares. One of the main tenets of competition law is: lower prices are good for consumers (in general), as long as service quality remains the same. With Uber in the mix, quality arguably increases beyond the sad status quo of smelly and difficult-to-hail cabs: for one, users now are able to know when and where their car arrives, quality control via Uber’s policies and check-ups is available, convenient electronic billing & dispute resolution exists, etc.

Let’s go back to the FTC’s public comments and see their take:

“Competition and consumer protection naturally complement and mutually reinforce each other, to the benefit of consumers. Consumers benefit from market competition, which creates incentives for producers to be innovative and responsive to consumer preferences with respect to price, quality, and other product and service characteristics. As the U.S. Supreme Court has recognized, the benefits of competition go beyond lower prices: ‘The assumption that competition is the best method of allocating resources in a free market recognizes that all elements of a bargain – quality, service, safety, and durability – and not just the immediate cost, are favorably affected by the free opportunity to select among alternative offers’.”

EU DG COMP

Former Competition Commissioner Neelie Kroes would agree wholeheartedly with the above, and indeed said in 2014 that she was “outraged at the decision by a Brussels court to ban Uber.” In her personal op-ed piece, published on the EU Commission’s web site under the catchy title “Crazy court decision to ban Uber in Brussels“, she poignantly had this to tell the Belgian Mobility Minister who signed off on the Uber ban:

“This decision is not about protecting or helping passengers – it’s about protecting a taxi cartel. The relevant Brussels Regional Minister is Brigitte Grouwels. Her title is “Mobility Minister”. Maybe it should be “anti-Mobility Minister”. She is even proud of the fact that she is stopping this innovation. It isn’t protecting jobs Madame, it is just annoying people!”

We wonder what would happen if Neelie Kroes were Kenyan government minister…

Kenya: Keep prices high and ‘foreign’ competition out?

The Kenyan Taxi Association does not see it that way, just like its D.C. counterpart did not some 3 years ago. However, D.C.’s streets are still full of old-fashioned cabs, and Uber — while popular — is still far from blowing out the light shone by the once-prized cabbie medallions…

Still, the Kenyan association claims that between 4,000 and up to 15,000 taxi drivers face job extinction due to lower prices charged by Uber, which has been active in Nairobi since the beginning of 2015. Again, the “lower price” argument is a red herring under even the most basic application of competition economics, which shows that innovation-based price competition is ultimately pro-competitive and good not only for the end consumer but also the industry’s development as a whole.

The Kenyan taxi-cab organisation not only claims that the livelihoods of its members are at stake, but also “questioned the protocols followed by the foreign investors behind Uber, saying they were not consulted before the service provider entered the market,” according to an article in the Kenyan Daily Nation. The association’s spokesman is quoted as saying: “We have loans to service, families to feed, children to educate and other responsibilities to cater for and we are not ready to leave the transport industry to a foreigner and render [ourselves] jobless while we are in a democratic republic.”

So in the end, the ‘unfair taxi competition’ argument devolves into xenophobia and mistrust. Sadder yet, Kenya’s Uber fight has now taken a violent turn: Yesterday, an Interior Ministry spokesman said that there had been reports of attacks on Uber drivers, which are being investigated.

AAT of course deplores the resort to violence and trusts that neither it nor the upcoming protests will impede the progress of competitiveness in Kenya, a country that otherwise prides itself on encouraging competition (see CNBC Africa video on “East African competitiveness”). The sole glimmer of hope we see consists of the closing line of the Daily Nation piece, which notes that “[t]he drivers have also promised to come up with their own version of Uber to connect taxi drivers in the country.” That is what innovation is all about: Uber innovates, others copy (be it Lyft or the Kenyan cabbies), and everyone is better off in the final analysis.

East-Africa & Antitrust: Enforcement of EAC Competition Act

By AAT guest author, Anne Brigot-Laperrousaz.

Introduction: Back in 2006…

The East African Community (the “EAC”) Competition Act of 2006 (the “Act”) was published in the EAC Gazette in September 2007. The Act was taken as a regulatory response to the intensification of competition resulting from the Customs Union entered into in 2005. This was the first of the four-step approach towards strengthening relations between member States, as stated in Article 5(1) of the Treaty Establishing the EAC.

Challenges facing the EAC

As John Oxenham, an Africa practitioner with advisory firm Pr1merio, notes, “10 years have passed since the adoption of the EAC Act, yet it remains unclear when (and if) the EAC will develop a fully functional competition law regime.”

The EAC Competition Authority (the “Authority”) was intended to be set up by July 2015, after confirmation of the member States’ nominees for the posts of commissioners. Unfortunately Rwanda, Uganda and Burundi failed to submit names of nominees for the positions available, and the process has become somewhat idle, leaving questions open as to future developments.

The main challenges facing the EAC identified by the EAC’s Secretariat is firstly, the implementation of national competition regulatory frameworks in all member States; and secondly, the enhancement of public awareness and political will[1].

The first undertaking was the adoption of competition laws and the establishment of competition institutions at a national level, by all member states, on which the sound functioning of the EAC competition structure largely relies.

Apart from Uganda, all EAC member States have enacted a competition act, although with important discrepancies as to their level of implementation at a national level.

The second aspect of the EAC competition project is the setting up of the regional Competition Authority, which was to be ensured and funded by all members of the EAC, under the supervision of the EAC Secretariat. Although an interim structure has been approved by member States, the final measures appear to be at a deadlock.

As mentioned, the nomination of the commissioners and finalisation of the setting up of the EAC Competition Authority came to a dead-end in July 2015, despite the $701,530 was set aside in the financial budget to ensure the viability of the institution[2]. It is widely considered, however, that this amount is still insufficient to ensure the functionality of the Competition Authority. Andreas Stargard, also with Pr1merio, points out that “[t]he EAC has been said to be drafting amendments to its thus-far essentially dormant Competition Act to address antitrust concerns in the region. However, this has not come to fruition and work on developing the EAC’s competition authority into a stable body has been surpassed by its de facto competitor, the COMESA Competition Commission.”

Furthermore, inconsistencies among national competition regimes within the EAC are an important impediment to the installation of a harmonised regional enforcement. Finally, international reviews as well as national doctrine and practice commentaries have highlighted the lack public sensitization and political will to conduct this project.

A further consideration, as pointed out by Wang’ombe Kariuki, Director-General of the Competition Authority of Kenya, is the challenge posed by the existence of the Common Market for Eastern and Southern Africa (“COMESA”).

Conclusion

The implementation of the EAC has not seen much progress since its enactment, despite its important potential and necessity[3]. It therefore remains to be seen how the EAC deals with the various challenges and whether it will ever become a fully functional competition agency.

A quick summation of the status of the national laws of the various EAC members can be seen below. For further and more comprehensive assessments of the various member states competition law regimes please see African Antitrust for more articles dealing with the latest developments.

The Tanzanian Fair Competition Act (the “FCA”) was enacted in 2003, along with the institution of a Commission and Tribunal responsible for its enforcement. The FCA became operational in 2005. Tanzania’s competition regime was analysed within the ambit of an UNCTAD voluntary peer review in 2012[4]. The UNCTAD concluded that Tanzania had overall “put in place a sound legal and institutional framework”, containing “some of the international best practices and standards”.

This report, however, triggered discussions on major potential changes to the FCA, which would impact, in particular, institutional weaknesses and agency effectiveness[5]. One of the most radical changes announced consisted in the introduction of criminal sanctions against shareholders, directors and officers of a firm engaged in cartel conduct[6], although there is no sign that this reform will be adopted.

Kenya, following a 2002 OECD report[7] and the European Union competition regulation model, replaced its former legislation with the 2010 Competition Act, which came into force in 2011, and established a Competition Authority and Tribunal. Under the UNCTAD framework, the 2015 assessment of the implementation of the recommendations made during a voluntary peer review conveyed in 2005[8] was generally positive. It was noted, however, that there was an important lack of co-operation between the Competition Authority and sectoral regulators, and that there was a need for clear merger control thresholds[9].

Burundi adopted a Competition Act in 2010, which established the Competition Commission as the independent competition regulator. To date, the Act has not yet been implemented, and accordingly no competition agency is in operation[10].

A 2014 study led by the Burundian Consumers Association (Association Burundaise des Consommateurs, “Abuco”) (which was confirmed by the Ministry of Trade representative) pointed to the lack of an operating budget as one of the main obstacles to the pursuit of the project[11].

Rwanda enacted its Competition and Consumer Protection Law in 2012, and established the Competition and Consumer Protection Regulatory Body.

As for Uganda, to date no specific legal regime has been put in place in Uganda as regards competition matters, although projects have been submitted to Uganda’s cabinet and Parliament, in particular a Competition Bill issued by the Uganda Law Reform Commission, so far unsuccessfully.

Footnotes:

[1] A Mutabingwa “Should EAC regulate competition?” (2010), East African Community Secretariat

[2] C Ligami, “EAC to set up authority to push for free, fair trade” (2015), The EastAfrican

[3] O Kiishweko, “Tanzania : Dar Praised for Fair Business Environment” (2015), Tanzania Daily News

[4] UNCTAD “ Voluntary Peer Review on competition policy: United Republic of Tanzania” (2012), UNCTAD/DITC/CLP/2012/1

[5] S Ndikimi, “The future of fair competition in Tanzania” (2013), East African Law Chambers

[6] O Kiishweko, “Tanzania: Fair Competition Act for Review’ (2012), Tanzania Daily News.

[7] OECD Global Forum on Competition, Contribution from Kenya, “ Kenya’s experience of and needs for capacity building/technical assistance in competition law an policy “ (2002), Paper n°CCNM/GF/COMP/WD(2002)7

[9] MM de Fays, “ UNCTAD peer review mechanism for competition law : 10 years of existence – A comparative analysis of the implementation of the Peer Review’s recommendations across several assessed countries” (2015)

We have previously, on African Antitrust, reported on South Africa’s first predatory pricing case in the Media 24 matter. In light, however, of the recent cases on exclusionary conduct — particularly predatory pricing, which has received significant attention from competition law agencies across a number of jurisdictions of late (see, for instance, the Paris Court of Appeals’ dismissal of the predatory pricing and exclusionary conduct allegations made against Google by an online maps rival. The Indian Competition Commission has also launched an investigation into alleged predatory pricing in the taxi industry, and the European Commission has launched investigations into predatory pricing in the potato-chips / crisps industry) — a more substantive evaluation of predatory pricing in South Africa is called for. The following article on predatory pricing, in light of the Media 24 case, neatly sets out and evaluates the landscape of predatory pricing in South Africa.

Predatory Pricing & the South African Competition Act: a False-Positive?

By Michael J. Currie

Intro & Summary

“From an antitrust perspective, predatory pricing is a particularly difficult problem with which to deal. If we are to prevent anticompetitive monopolization, it is a strategy that must not be permitted. The paradox, however, is that such a pricing strategy is virtually indistinguishable from the very sort of aggressive competitive pricing we wish to encourage.”

D L Kaserman and J W Mayo, ‘Government and Business: The Economics of Antitrust and Regulation’ (1995) Fort Worth, TX: Dryden Press at 128

In September 2015, the Competition Tribunal (“Tribunal”), for the first time in South Africa’s sixteen-year history of competition-law enforcement found, in the Media 24 case that the respondent had engaged in predatory pricing in contravention of the South African Competition Act, 89 of 1998 (“Act”).

The Media 24 case, despite being dragged out for nearly six years, was set to be the leading jurisprudence on the laws pertain to predatory pricing, and in particular, how Section 8(d)(iv) of the Act would be interpreted and applied by the Tribunal. The finding by the Tribunal was, however, based on Section 8(c) of the Act, which is a broader ‘catch-all’ provision, and left some important questions as to the interpretation of Section 8(d)(iv) unanswered. Most notably, whether or not Section 8(d)(iv) permits complainants to utilise cost measurement standards other than Average Variable Costs (“AVC”) or Marginal Costs (“MC”) to prove that a dominant firm has engaged in predatory pricing in contravention of the provision.

Having said that, however, the Media 24 case provides some insight as to the precise relationship between Sections 8(d)(iv) and 8(c) of the Act as they relate to predatory pricing, and may have offered, by way of certain obiter remarks, an indication as to how the Tribunal may interpret and apply Section 8(d)(iv) of the Act in the future.

Continue reading the full article, an AAT exclusive, in PDF format:

Continuing the original AAT series, ECONAfrica, Peter O’Brien addresses the WTO’s upcoming MC10 conference.

From 15-18 December Nairobi will host the 10th Ministerial Conference (MC10) of the World Trade Organization (WTO). This will be a meeting of many firsts. Till now, no sub-Saharan African country had hosted a Ministerial Conference organised by the WTO. Nairobi will bring into force the Trade Facilitation Agreement (TFA), the first occasion in the now 21 year history of WTO that a new agreement has been signed (all others were established at the inception of WTO). This is the first MC to take place against the backdrop of an agreement in Africa, concluded this year, to work for a continent wide area of free trade. Today more than one quarter (43 countries in total) of all WTO Members (more than 160) are African. Moreover, the Accession Package for Liberia was agreed in Geneva on 6 October, and it can be expected that it too will join in the course of 2016.

Apart from celebrating the firsts, are there any reasons for business in Africa to pay attention to events in Nairobi? The answer is an emphatic yes:

The TFA is the one WTO agreement that promises real advantages on the logistics of trade. Detailed studies have shown that, on average, the sheer movement of goods within Africa accounts for roughly one fifth of all costs. Serious steps to cut those costs, which is what TFA is about, represent a win/win for producers, traders, consumers and indeed the public authorities. Since Africa is the region of the world where intra-trade (transactions among African countries themselves) is by far the lowest, and where most national markets are small, the gains from logistics savings are potentially huge.

The TFA will commit WTO Members to help the least developed countries, a group of over 30 States of whom the majority are African. For the first time, there are straight advantages to be obtained without a condition of reciprocity. Funding, technical assistance, streamlining of trade administration, are just some of the things that can be expected. The TFA allows governments and business together to formulate their requests, so this is the chance to utilize an organized offer of support.

MC10 will seek to reinforce the whole network of disciplines concerned with non-discrimination and competition that constitute the core of WTO agreements. That progress is very positive for the growth of competitive markets on the continent.

The meeting will be attended by numerous international and regional observer organizations from the private sector, as well as by non-governmental organizations (NGOs) whose normal activities are overwhelmingly directed towards improving trade and welfare in African countries. Their presence serves to strengthen the lobby for growth and welfare improvement.

In the world of yesterday, tariffs and quantitative limitations dominated trade negotiations. In tomorrow’s world, the critical subjects are technical barriers to trade (meaning formal legal resolutions that control trade for purposes of national security, public health and so on), voluntary norms and standards (which in practice frequently acquire a market force equivalent to a legal provision), and a host of other regulatory issues that determine who will be best placed in the market.

More or less all African countries, with the partial exception of South Africa, have always been on the receiving end of these instruments. Africa has thus far played a very minor role in shaping “the rules of the international competitive game.”But with the continent now the fastest-growing region in the world economy, with the race for its natural resources continuing (despite the current lows in resource prices), with the ongoing investments (from within the continent and without), and the steady improvements in governance observable in the majority of countries, Africa is well placed to make its voice heard.

Nairobi and the MC10 offer the ideal stage on which the continent can begin its future path as one of the designers of competitive change.

Professional fees for advocates in Kenya are set by the Chief Justice under the Advocates Act Chapter 16 of the Laws of Kenya. Part IX Section 44 provides that the Chief Justice may by order prescribe and regulate in such manner as he/she thinks fit the remuneration of advocates in respect of all professional business, whether contentious or non-contentious. Sub-section (2) also provides that the Chief Justice may prescribe a scale of rates of commission or percentage in respect of non-contentious business.

Professional fees for advocates in Kenya are set by the Chief Justice under the Advocates Act Chapter 16 of the Laws of Kenya. Part IX Section 44 provides that the Chief Justice may by order prescribe and regulate in such manner as he/she thinks fit the remuneration of advocates in respect of all professional business, whether contentious or non-contentious. Sub-section (2) also provides that the Chief Justice may prescribe a scale of rates of commission or percentage in respect of non-contentious business. We are referring to the “phased” implementation of the 2009

We are referring to the “phased” implementation of the 2009  According to news reports, Mr. Patel announced today (Thursday), that the criminalisation of the price-fixing cartel offence would henceforth be enforced. Section 73A will be gazetted tomorrow, 22 April 2016, and hold the force of law from 1 May 2016. BDLive also

According to news reports, Mr. Patel announced today (Thursday), that the criminalisation of the price-fixing cartel offence would henceforth be enforced. Section 73A will be gazetted tomorrow, 22 April 2016, and hold the force of law from 1 May 2016. BDLive also  We live in the era of the

We live in the era of the

From 15-18 December Nairobi will host the 10th Ministerial Conference (MC10) of the World Trade Organization (WTO). This will be a meeting of many firsts. Till now, no sub-Saharan African country had hosted a Ministerial Conference organised by the WTO. Nairobi will bring into force the Trade Facilitation Agreement (TFA), the first occasion in the now 21 year history of WTO that a new agreement has been signed (all others were established at the inception of WTO). This is the first MC to take place against the backdrop of an agreement in Africa, concluded this year, to work for a continent wide area of free trade. Today more than one quarter (43 countries in total) of all WTO Members (more than 160) are African. Moreover, the Accession Package for Liberia was agreed in Geneva on 6 October, and it can be expected that it too will join in the course of 2016.

From 15-18 December Nairobi will host the 10th Ministerial Conference (MC10) of the World Trade Organization (WTO). This will be a meeting of many firsts. Till now, no sub-Saharan African country had hosted a Ministerial Conference organised by the WTO. Nairobi will bring into force the Trade Facilitation Agreement (TFA), the first occasion in the now 21 year history of WTO that a new agreement has been signed (all others were established at the inception of WTO). This is the first MC to take place against the backdrop of an agreement in Africa, concluded this year, to work for a continent wide area of free trade. Today more than one quarter (43 countries in total) of all WTO Members (more than 160) are African. Moreover, the Accession Package for Liberia was agreed in Geneva on 6 October, and it can be expected that it too will join in the course of 2016.