Key competition-law conference features dedicated panel discussion on African antitrust developments

By Michael-James Currie

The 54th annual American Bar Association Antitrust Spring Meeting was held in Washington, D.C., during the second week of April 2016 and the AAT editors were there to ensure that we provide our readers with an update on the latest developments in relation to African antitrust issues, discussed during a panel held last Friday.

Given that mergers hit a global all-time high last year with the total value of transactions amounting to over USD 4.6 trillion, merger control is certainly at the forefront of many antitrust practitioners. The interest in mergers and acquisitions has perhaps gained even further attention in light of the announcement this week that the USD160 billion Pfizer/Allergan global mega-deal has been officially abandoned, despite the transaction having already been filed before all the relevant competition agencies around the world. While the Pfizer/Allergan deal was called off as a result of new tax laws and therefore not as a result of antitrust issues directly, the deal did put multinational mega-deals firmly in the spotlight.

The Pfizer/Allergan deal is not the only mega-deal that faced significant government opposition. It was announced this week that Halliburton’s takeover of Baker Hughes, in a deal valued at USD 25 billion, is going to be strongly opposed by the U.S. DOJ.

It is, however, not only the U.S. Government that is having a significant impact on multinational deals, as evidenced by the Anbang Insurance and Starwood Hotels & Resorts deal, valued at USD 14 billion, which has also been abandoned after mounting pressure by the Chinese government.

From an African perspective, the South African Competition Commission just last week extended its investigation in the USD 104 billion SABMiller and Anheuser-Busch InBev merger. It is widely suspected that the request for the extension is due to intervention by the Minister of Economic Development, in relation to public interest grounds. Although there is no suggestion at this stage that Minister Patel is opposing the deal, the proposed intervention does highlight bring into sharp focus the fact that multinational mega-deals face a number of hurdles in getting the deal done.

‘Getting multinational deals through’ is a hot topic at the moment amongst antitrust practitioners and is and the ABA thought it beneficial to have a panel discussion dedicated purely to merger control issues across African jurisdictions. In particular, the panel addressed some of the key issues which merging parties need to consider, including inter alia issues relating to harmonisation across agencies, the role of public interest considerations, prior implementation and the need for upfront substantive economic assessments.

The panel consisted of a varied mix of panellists from both private practice and government, and included Pr1merio director John Oxenham (he is also a founding partner at South African based law firm Nortons Inc.), economist and former Commissioner of the COMESA Competition Commission (COMESA CC) Rajeev Hasnah (Rajeev was also a former commissioner of the Mauritius Competition Commission and is an economist for Pr1merio), manager of the South African Competition Commission office, Wendy Ndlovu, and Kenyan based external counsel Anne Kiunuhe (Anne practices at the law firm Anjarwalla & Khanna).

The panellists were tasked with addressing a variety of topics: we summarise below some of the key issues which the panellists highlighted, which merging parties, practitioners and antitrust agencies themselves (amongst whom Tembikosi Bonakele, the South African Competition Commissioner was present in the panel audience) should be cognisant of in relation to merger control in Africa.

John Oxenham

John pointed out that from a South African perspective, mergers undergo a robust evaluation by the Competition Authorities and that although the investigation of most large mergers is completed within 60-70 days, the fact that the Commission may request the Competition Tribunal for an extension of up to 15 business days at a time, may result in the investigation of certain mergers taking considerably longer. The risk of a merger being delayed is increased significantly due to the level of third party interventionism, particularly ministerial intervention on public interest grounds.

John advised that merging parties should consider the impact that a particular merger will have on the public-interest grounds upfront to avoid delays in the investigation period as a result of further requests for information from the Commission, or may even amount to an incomplete filing.

In respect of substantive economic assessments, John pointed out that a number of jurisdictions, including South Africa, Namibia, Zambia and to a lesser extent Botswana, requires a substantive upfront economic assessment. In this regard the South African Competition Commission is perhaps the most robust in its economic evaluation of a merger in light of the resources dedicated to its own in-house economic department as well as utilising external experts when necessary. John also highlighted the fact that the South African Competition Authorities rely on oral testimony and expert witnesses are often subjected to substantial and lengthy examination and cross examination before the Competition Tribunal.

On the topic of gun-jumping or prior implementation, John mentioned that the following jurisdictions are examples of countries which do not require notification prior to implementing the transaction – in other words, they are not suspensory:

- Malawi

- Senegal

- Mauritius

Whereas the following countries do require notification prior to implementation (suspensory merger control jurisdictions):

- South Africa

- Swaziland

- Zambia

- Botswana

On harmonisation, John confirmed that in relation to public interest considerations in merger control, the South African competition authorities play a leading role on the African continent and pointed out that in addition to Kenya and Tanzania, Namibia also considers public interest considerations and that there is a substantial amount of collaboration and information sharing between the South African and Namibian competition authorities, as was the case in the Walmart/Massmart deal.

Despite the information sharing between agencies, John confirmed that there are rules in place to protect confidential and legally privileged information and that the South African competition authorities are cognisant and respectful of these provisions.

Rajeev Hasnah

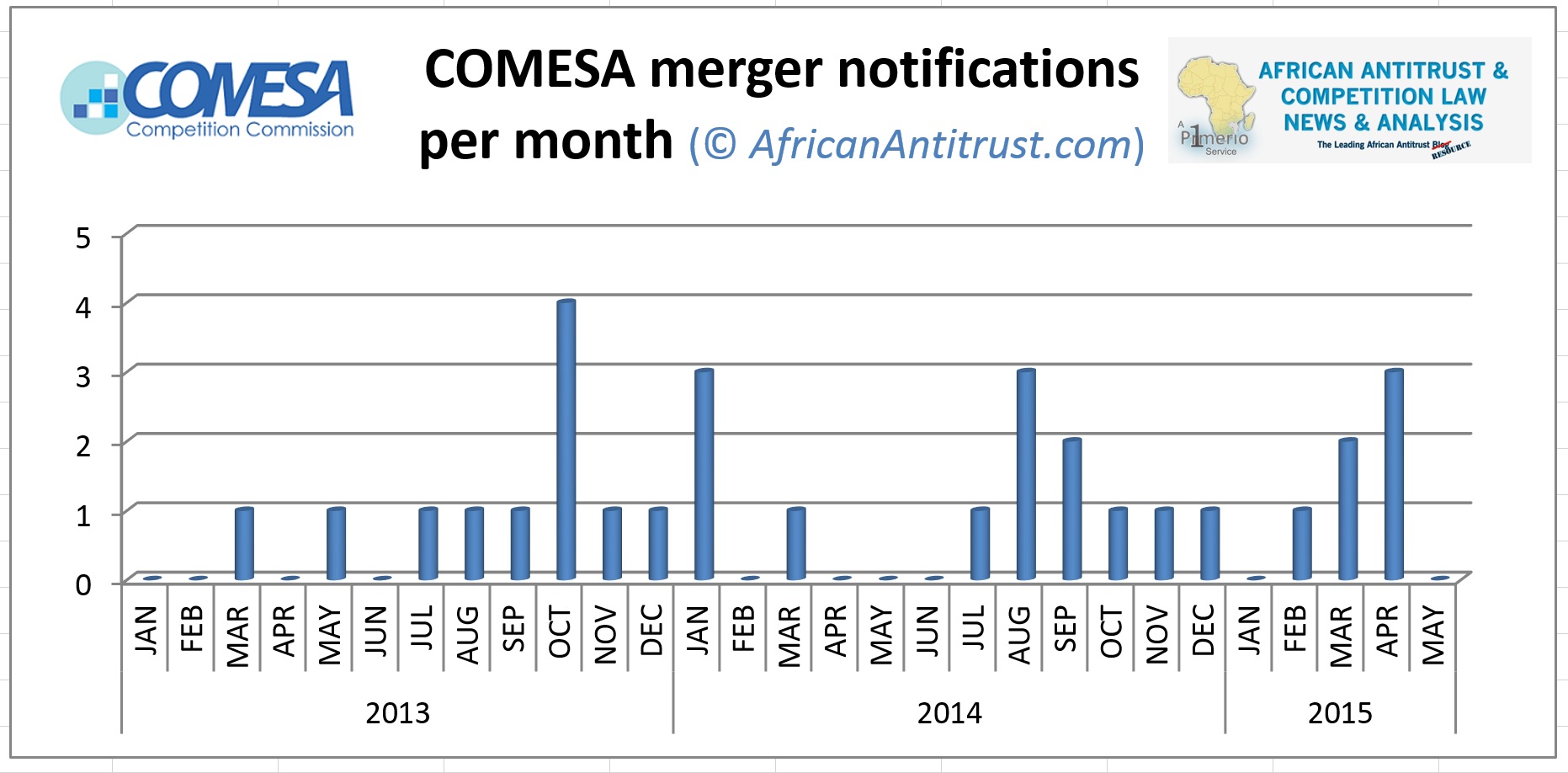

Rajeev noted the significant progress which the COMESA CC has made in relation to merger control by publishing financial thresholds for mandatorily notifiable transactions and specified filing fees, as well as publishing guidelines which clarify when a merger will have a sufficient regional dimension to fall within the COMESA CC’s jurisdiction.

On the topic of harmonisation, Rajeev discussed the challenges due to a lack of harmonisation between COMESA and its member states and noted that COMESA does not have exclusive jurisdiction in the cases which do fall within its jurisdiction. Parties, therefore, may find themselves being required to file a merger both before the COMESA CC as well as before the respective national authorities. A further challenge facing the COMESA CC is that there are 19 member states and consequently, the relevant geographic market is significant. Accordingly, often the national authorities are best placed to evaluate a merger and will therefore defer the evaluation of the merger to the relevant national authority.

On the role of economic assessments, Rajeev stated that an economic assessment underlies any merger evaluation and that both the Mauritius Competition Commission and the COMESA Competition Commission conducts a comprehensive economic assessment of a merger.

Wendy Ndlovu

When asked on what role public interest considerations play in merger control in terms of the South African competition regime, Wendy indicated that the framework of the Competition Act specifically requires the competition authorities to consider the impact that a merger may have on the four specified public interest provisions contained in the Act. Wendy confirmed that an evaluation of public interest considerations may both justify a merger despite the merger likely being likely to cause a substantial lessening or prevention of competition in the market, alternatively, public interest considerations may lead to a prohibition or the imposition of conditions on a merger which raises no competition law concerns and may in fact be pro-competitive.

Wendy recognised that there is a need, however, for greater certainty in respect to the manner in which the South African authorities evaluate public interest considerations and pointed out that the Competition Commission is likely to finalise and publish its guidelines on the public interest assessment in an effort to promote greater certainty.

On prior the issue of prior implementation, Wendy pointed out that merging parties need to be mindful of the consequences of gun-jumping and noted that the South African Competition Tribunal has imposed administrative penalties, as in the Netcare case, on parties for failing to notify a mandatorily notifiable transaction.

Anne Kiunuhe

Anne discussed the Competition Authority of Kenya’s (CAK) willingness to focus not only on merger control but has also identified the CAK’s increasing tendency to investigate and prosecute firms engaged in restrictive practices (as demonstrated by the recent dawn raids conducted by the CAK in the fertiliser industry). Despite the CAK’s growing confidence, Anne pointed out that in respect of merger control, the CAK is open to and in fact often relies on precedent from foreign jurisdictions when evaluating a merger. In particular, Anne noted that public interest grounds are specifically considered during the merger review procedure and that in this respect, the CAK largely takes the lead from the South African competition authorities.

From a practical perspective, Anne mentioned that the CAK usually requests a meeting with the merging parties soon after a transaction has been notified, and that usually representatives from the merging parties, along with local external legal counsel, should be present. The CAK prefers that the representatives present should be the best placed to answer or address the CAK’s queries. This often necessitates representatives from the parent company being present as opposed to representatives from the subsidiary entities only.

The direct contact between the CAK and the merging parties is quite different from the manner in which the COMESA CC evaluates mergers where the consideration of a merger is done solely on the papers and any communication between the COMESA CC and the merging parties is done through the merging parties’ local external counsel.

As to legislative developments, Anne pointed out that the merger regulations in Kenya now provide that for purposes of establishing a “change of control”, it is sufficient if the acquiring firm is able to materially influence the commercial decisions of the target firm. Accordingly, the acquisition of a minority shareholding for instance may constitute a change of control if the holders of such shares may for instance exercise veto rights.

On COMESA, Anne mentioned that the COMESA CC permits merging parties to seek a comfort letter when unsure as to whether a merger requires filing and that the use of comfort letters has been rather prevalent.

Conclusion

The role of public interest considerations in merger control was a dominant focus point throughout the panel discussion due to this unique aspect in a growing number of African jurisdictions merger control provisions.

Please click on the following link to access a an article on the role of public interest considerations in merger control in South Africa, which addresses in particular, the impact of ministerial intervention in merger proceedings and the concomitant impact which such intervention has on the costs, timing and certainty of merger proceedings.